Economic Globalization

Over the last fifty years, the world economy has experienced rapid economic growth as the world had become more economically interconnected, especially after the collapse of the Soviet Union in 1991. Advances in information technology have driven economic innovation and spawned many new businesses and industries.

Learning Objectives

Examine the world economy since the 1970s.

Analyze the causes, concepts, and consequences of globalization.

Identify developing global political, social, and technological structures.

Key Terms / Key Concepts

Bretton Woods system: a monetary management system that established the rules for commercial and financial relations among the United States, Canada, Western Europe, Australia, and Japan in the mid-20th century

European Central Bank: consisting of 19 European Union (EU) member states, the central bank for the euro that administers monetary policy of the eurozone

European Council: the institution of the European Union that comprises the heads of state or government of the member states, along with the President of the European Council and the President of the European Commission, charged with defining the EU’s overall political direction and priorities

European Commission: an institution of the European Union responsible for proposing legislation, implementing decisions, upholding the EU treaties, and managing the day-to-day business of the EU

European Economic Community: a regional organization that aimed to bring about economic integration among its member states. It was created by the Treaty of Rome of 1957

immigration: the international movement of people into a destination country where they do not possess citizenship to settle or reside there, especially as permanent residents or naturalized citizens, sometimes to take up employment as migrant workers or temporarily as foreign workers

International trade: the exchange of capital, goods, and services across international borders or territories

Maastricht Treaty: a treaty undertaken to integrate Europe and signed in 1992 by the members of the European Community

modernization theory: a theory used to explain the process of modernization within societies using a model of progressive transition from pre-modern or traditional societies to modern society; a theory that assumes that with assistance, so-called traditional societies can be developed in the same manner as currently developed countries

Schengen Area: an area composed of 26 European states that have officially abolished passport and any other type of border control at their mutual borders, which mostly functions as a single country for international travel purposes with a common visa policy

supranationalism: a type of multinational political union where negotiated power is delegated to an authority by governments of member states

Globalization

Since the end of World War II in 1945, the world has experienced unparalleled economic and population growth. The world's population jumped from 2.5 billion people in 1950 to 7.5 billion people in 2020. The economies of the world have become increasingly integrated into a global economic system, as large corporations such a McDonald's and Walt Disney operate their businesses in multiple countries worldwide. The Consumer Revolution, which began in the United States in the 1920s, has spread around the world, resulting in the creation of a global popular culture based on consumers' demands for various goods (i.e., clothing, music, video games).

In the decades following World War II in the 1950s and 1960s the world economy recovered rapidly from the war's devastation. The strong United States' economy with its vast financial resources provided the capital investment to rebuild the shattered economies of its allies in the Cold War. Unlike Europe, the United States during World War II had not suffered from the destruction of its cities, factories, roads, and railroads. In fact, the United States came out of this war economically stronger since the war had boosted industries and wages due to the demand for war materials. American consumers after the war were eager to spend their rising wages on consumer goods. In the United States and its Cold War allies Keynesian economic theory shaped policy makers' approach to handling the economy in this period, as a result of the Great Depression.

These countries all were “Welfare States”; the state provided a “safety net” for its poorest citizens by providing them with supplementary incomes as well as food, housing, and healthcare. The state also boosted employment and wages through public works projects and support for labor unions. These policies served to ensure that consumers had sufficient incomes to maintain demand in this highly regulated market economy.

the United States also promoted international trade through the International Monetary Fund and World Bank, which served to stabilize currencies and provide funds for capital investments among US allies. The United States had created and funded these organizations at the close of World War II to foster the rebuilding of the world economy (the so-called “Bretton Wood System”).

In this postwar period the US also opposed trade protectionism to lessen trade barriers between nations. For example, the United States Congress in 1962 passed the Trade Expansion Act, which authorized the US president to negotiate tariff agreements between the US and other nations. This act resulted in a series of talks (the Kennedy Round) between 1964 and 1967 among nations in Geneva, Switzerland who were involved in the General Agreement on Tariffs and Trade (GATT) negotiation sessions. These talks resulted in the United States reducing its tariffs by at least 35%. The US, however, didn't require “developing” nations in Asia, Africa, and Latin America to reduce their tariffs. Consequently, these talks boosted exports from these countries to the United States and Western Europe, while these countries could protect their own emerging industries from competition from imports from the United States and Western Europe through high tariffs (“import substitution industrialization”).

The “Eastern Bloc” countries (the Soviet Union and Eastern Europe) at this time also experienced rapid economic growth under a command economy. This period witnessed the mass movement of people in these states from rural areas to work in new state-owned factories. The apparent success of these countries in spurring rapid economic growth was a reason why many Third World countries embraced Soviet Marxist-Leninism.

In the 1970s both the “Eastern Bloc” and the “Free World” (the US and its allies) experienced economic crises as economic growth stalled and commodity prices surged resulting in high inflation. In this period oil prices increased since demand for oil exceeded supply.

In 1960, a number of nations rich in oil resources formed the Organization of Petroleum Exporting Countries (OPEC) as a cartel to regulate world oil supplies. Many members of this cartel were Muslim countries (i.e., Saudi Arabia, Iraq, Libya, Iran); after the Yom Kippur War in 1973, these counties imposed an oil embargo to protest American support for Israel in the war between Israel and Muslim Egypt. Consequently, in the mid-1970s oil prices rose dramatically and resulted in a worldwide recession (economic downturn). In 1979, oil prices spiked again due to the Iranian Revolution, since Iran was a member of OPEC and its revolution posed a threat to the stability of the Persian Gulf countries that provided much of the world's oil supply. High oil prices resulted in rampant inflation worldwide since the world's production and transportation of goods all largely required oil to create energy through its factories, railroads, trucks, and planes. High oil costs, therefore, increased costs for all goods. Since consumers were thus paying higher prices for basic necessities such as gas and groceries, they were less likely to purchase non-essential consumer goods, and demand for these goods therefore declined. This “energy crisis” thus had the effect of slowing and even decreasing economic growth in countries with a market economy.

The Eastern Bloc countries in the 1970s with their command economies also witnessed slowing economic growth in this period in sharp contrast to the rapid industrialization of the previous two decades. By the 1980s the standard of living in the Eastern Bloc countries had become substantially lower than the standards of living in Western Europe, in which countries such as West Germany were flourishing by exporting manufactured goods to consumers, especially in the United States. This disparity between the economies of the Eastern Bloc and Western Europe was a factor in the collapse of the Communist regimes by the end of the 1980s.

In the 1980s the United States under the leadership of President Ronald Reagan and the United Kingdom under Prime Minister Margaret Thatcher rejected Keynesian economic theory and instead embraced the economic theories of the Chicago School of Economics, also known as Neoliberalism. According to this economic theory, “unnecessary” government regulations and high tax rates hindered capital investment, which was the key to economic growth, not Keynes’s consumer demand. Critics of this economic theory viewed it as a return to the failed Laissez-faire policy of the past. Reagan and Thatcher's administrations maintained, however, that this approach to the economy would reinvigorate their countries’ stagnant economies.

In the 1980s the governments of both the United States and the United Kingdom reduced taxes and eliminated government regulations. In the United Kingdom, the Conservative (Tory) government privatized industries that had been previously nationalized by the government under the Socialist Labour Party. The vibrant economic growth of the United States and the United Kingdom in the 1980s convinced even formally Socialist parties, such as the Labour Party and Germany's Social Democratic Party, to embrace some Neoliberal policies in the 1990s, including free trade and the reduction of government regulations.

The world’s economic growth in the 1980s and 1990s was also a result of the dramatic transformation of “Communist” China as the country after 1979 embraced a market economy. The new leader of the Communist Party, Deng Xiaoping began a program of privatizing state run enterprises and allowed American and European companies to build factories in China, as well as employ Chinese labor in exchange for China's access to their technology. Deng Xiaoping maintained that this new policy would modernize the Chinese economy and improve the standard of living for the Chinese people. In the decades that followed, millions of Chinese citizens migrated to the cities to work in these new factories to produce goods so as to export primarily to the United States and Europe. Incomes in China for workers did steadily increase along with the emergence of a prosperous Chinese middle class. American and European companies with factories in China generated huge profits since the cost of labor was so much lower in China than in the United States and Europe. By the second decade of the 21st century, China had emerged as the second largest economy in the world, after the United States.

The adoption of Neoliberal policies by countries around the world has been quite controversial. Countries adopting these policies have often reduced taxes without necessarily reducing government spending, resulting in large amounts of government debt. Consequently, in the 1990s many countries in Latin America (i.e., Mexico) and Asia (i.e., Indonesia) declared bankruptcy and relied on loans from the IMF to stay afloat. The US supported IMF has imposed “austerity measures” as the price of receiving these loans, which required these countries to slash government spending as a way to balance their governments' budgets.

Critics of these austerity programs have pointed out that millions of people have lost their government jobs, as well as food, housing, and healthcare, as a result of the budget measures that governments have had to take after accepting IMF loans. Ironically, the United States’ government debt has also skyrocketed since the 1980s, but investors in the United States and around the world have continued to finance this tremendous debt by purchasing US government bonds, which is a way to avoid the austerity measures imposed on other nations.

The elimination of government regulations based on Neoliberal economic theory has also reportedly played a role in a series of spectacular, worldwide stock market collapses in and around 1990, 2000, and 2008. Critics of Neoliberalism have pointed out that the absence of proper government regulation of stock markets fueled risky speculation that resulted in these financial disasters. These critics have also pointed out that Neoliberal policies have resulted in rising inequality. Since the 1980s incomes across the world have risen substantially, but so has the percentage of wealth owned by a very small percentage of the world’s population (the so-called “one percent”). Lower tax rates on high income earners have enabled the very wealthy to accumulate more of the world’s total wealth.

The European Union

The political and economic integration of Western Europe since World War II, as well as much of Eastern Europe after the Cold War, has stimulated worldwide economic growth and globalization. The European Coal and Steel Community (ECSC) was born from the desire to prevent future European conflicts following the devastation of World War II. The European Coal and Steel Community (ECSC) was an international organization unifying certain continental European countries after World War II; it was formally established in 1951 by the Treaty of Paris, signed by Belgium, France, West Germany, Italy, the Netherlands, and Luxembourg. The ECSC was the first international organization based on the principles of supranationalism and would ultimately pave the way for the European Union.

The ECSC was first proposed by French foreign minister Robert Schuman on May 9, 1950. His declared aim was to make future wars among the European nations unthinkable due to higher levels of regional integration, with the ECSC as the first step towards that integration. The treaty would create a common market for coal and steel among its member states, which served to neutralize competition between European nations over natural resources used for wartime mobilization, particularly in the Ruhr. The Schuman Declaration that created the ECSC had distinct aims: It would mark the birth of a united Europe, make war between member states impossible, encourage world peace, and transform Europe incrementally, which would lead to the democratic unification of two political blocks separated by the Iron Curtain. Its aims also included creating the world’s first supranational institution, the world’s first international anti-cartel agency, and a common market across the Community. Its first aim was to revitalize the entire European economy by similar community processes, starting with the coal and steel sector. It would then improve the world economy, as well as the economies of developing countries, such as those in Africa.

In West Germany, Schuman kept close contact with the new generation of democratic politicians. Karl Arnold, the Minister President of North Rhine-Westphalia, the province that included the coal and steel producing Ruhr, was initially spokesman for German foreign affairs. He gave several speeches and broadcasts on a supranational coal and steel community at the same time as Schuman began to propose the Community in 1948 and 1949.

The Social Democratic Party of Germany, despite support from unions and other socialists in Europe, decided it would oppose the Schuman plan. This party claimed that a focus on integration would override the party’s prime objective of German reunification and thus empower ultra-nationalist and Communist movements in democratic countries. The party also thought the ECSC would end any hopes of nationalizing the steel industry and encourage the growth of cartel activity throughout a newly conservative-leaning Europe. Younger members of the party like Carlo Schmid were, however, in favor of the Community and pointed to the long tradition of socialist support for a supranational movement.

In France, Schuman gained strong political and intellectual support from all sectors, including many non-communist parties. Former French president, Charles de Gaulle, then out of power, had been an early supporter of linking European economies on French terms and spoke in 1945 of a “European confederation” that would exploit the resources of the Ruhr. However, he opposed the ECSC, deriding it as an unsatisfactory approach to European unity. He also considered the French government’s approach to integration too weak and feared the ECSC would be hijacked by other nation’s concerns. De Gaulle felt that the ECSC had insufficient supranational authority because the Assembly was not ratified by a European referendum, and he did not accept Raymond Aron’s contention that the ECSC was intended as a movement away from U.S. domination. Consequently, de Gaulle and his followers in the Rally of the French People (RPF) voted against ratification in the lower house of the French Parliament.

Despite these reservations and attacks from the extreme left, the ECSC found substantial public support. It gained strong majority votes in all 11 chambers of the parliaments of the six member states, as well as approval among associations and European public opinion. The 100-article Treaty of Paris, which established the ECSC, was signed on April 18, 1951, by “the inner six”: France, West Germany, Italy, Belgium, the Netherlands, and Luxembourg. On August 11, 1952, the United States was the first non-ECSC member to recognize the Community and stated it would now deal with the ECSC on coal and steel matters, establishing its delegation in Brussels.

First Institutions

The ECSC was run by four institutions: a High Authority composed of independent appointees, a Common Assembly composed of national parliamentarians, a Special Council composed of national ministers, and a Court of Justice. These would ultimately form the blueprint for today’s European Commission, European Parliament, the Council of the European Union, and the European Court of Justice.

The High Authority (now the European Commission) was the first-ever supranational body that served as the Community’s executive. The President was elected by the eight other members. The nine members were appointed by member states (two for the larger three states, one for the smaller three), but they were meant to represent the common interest rather than their own states’ concerns. The governments of the member states were represented by the Council of Ministers, the presidency of which rotated between each state every three months in alphabetical order. The task of this body was to harmonize the work of national governments with the acts of the High Authority and issue opinions on the work of the Authority when needed.

The Common Assembly, now the European Parliament, was composed of 78 representatives. The Assembly exercised supervisory powers over the executive. The representatives were to be national members of Parliament (MPs) elected by their Parliaments to the Assembly, or they were to be directly elected. The Assembly was intended as a democratic counterweight and check to the High Authority. It had formal powers to sack the High Authority following investigations of abuse.

The European Economic Community

The European Economic Community blossomed following the successful establishment of the European Coal and Steel Community, mainly from further regional integration. The European Economic Community (EEC) was a regional organization that aimed to integrate its member states economically. It was created by the Treaty of Rome of 1957. Upon the formation of the European Union (EU) in 1993, the EEC was incorporated and renamed as the European Community (EC). In 2009, the EC’s institutions were absorbed into the EU’s wider framework and the community ceased to exist.

After the establishment of the ECSC in 1951, two additional communities were proposed: a European Defense Community and a European Political Community. Both of these were meant to further regional integration. While the new treaty for the political community was drawn up by the Common Assembly, the ECSC parliamentary chamber, the proposed defense community under the proposed treaty was rejected by the French Parliament. ECSC President Jean Monnet, a leading figure behind the communities, resigned from the High Authority in protest and began work on alternative communities based on economic integration rather than political integration.

After the Messina Conference in 1955, Paul Henri Spaak was given the task of preparing a report on the idea of a customs union. Together with the Ohlin Report, the so-called Spaak Report would provide the basis for the Treaty of Rome. In 1956, Spaak led the Intergovernmental Conference on the Common Market and Euratom at the Val Duchesse castle. The conference led to the signature on March 25, 1957, of the Treaty of Rome, establishing a European Economic Community.

Creation and Early Years

The Treaty of Rome created new communities, the European Economic Community (EEC) and the European Atomic Energy Community (EURATOM, or sometimes EAEC). The EEC created a customs union, while EURATOM promoted cooperation in the sphere of nuclear power.

One of the first important accomplishments of the EEC was the establishment in 1962 of common price levels for agricultural products. In 1968, internal tariffs between member nations were removed on certain products. These accomplishments occurred despites some initial opposition. The formation of these communities had been met with protest due to a fear that state sovereignty would be infringed. Another crisis was triggered in regards to proposals for the financing of the Common Agricultural Policy (CAP), which came into force in 1962. The previous period whereby decisions were made by unanimity had come to an end, and majority voting in the Council had taken effect. Then French President Charles de Gaulle’s opposition to supranationalism and fear of the other members challenging the CAP led to an empty-chair policy in 1965 in which French representatives were withdrawn from the European institutions until the French veto was reinstated. Eventually, the Luxembourg Compromise of January 29, 1966, instituted a gentlemen’s agreement permitting members to use a veto on issues of national interest.

On July 1, 1967, the Merger Treaty came into force, combining the institutions of the ECSC and EURATOM into that of the EEC. Collectively, they were known as the European Communities. The Communities still included independent personalities, although they were increasingly integrated. Future treaties granted the Community new powers beyond simple economic matters, edging closer to the goal of political integration and a peaceful, united Europe.

Enlargement and Elections

The 1960s saw the first attempts at enlargement of participants. In 1961, Denmark, Ireland, Norway, and the United Kingdom applied to join the three Communities. However, President Charles de Gaulle saw British membership as a Trojan horse for US influence and vetoed membership, and the applications of all four countries were suspended. The four countries resubmitted their applications on May 11, 1967, and with Georges Pompidou succeeding Charles de Gaulle as French president in 1969, the veto was lifted. Negotiations began in 1970 under the pro-European government of UK Prime Minister Sir Edward Heath, who had to deal with disagreements relating to the CAP and the UK’s relationship with the Commonwealth of Nations. Nevertheless, two years later the accession treaties were signed, and Denmark, Ireland, and the UK joined the Community effective January 1, 1973. The Norwegian people finally rejected membership in a referendum on September 25, 1972.

The Treaties of Rome stated that the European Parliament must be directly elected; however, this required the Council to agree on a common voting system first. The Council procrastinated on the issue and the Parliament remained appointed. Charles de Gaulle was particularly active in blocking the development of the Parliament, with it only being granted budgetary powers following his resignation. Parliament pressured for agreement and on September 20, 1976, the Council agreed part of the necessary instruments for election, deferring details on electoral systems that remain varied to this day. In June 1979, during the tenure of President Roy Jenkins, European Parliamentary elections were held. The new Parliament, galvanized by a direct election and new powers, started working full-time and became more active than previous assemblies.

Maastricht Treaty

Towards Maastricht

The EEC continued to expand its membership in the 1980s. Greece applied to join the Community on June 12, 1975, following the restoration of its democracy, after a brief period of military dictatorship (1967-1974). Greece joined the Community effective January 1, 1981. Similarly, and after their own democratic restorations, Spain and Portugal applied to the communities in 1977 and both effectively joined on January 1, 1986. In 1987, Turkey formally applied to join the Community and began the longest application process for any country. With the prospect of further enlargement and a desire to increase areas of cooperation, the Single European Act was signed by foreign ministers in February 1986. This single document dealt with the reform of institutions, extension of powers, foreign policy cooperation, and the single European market. It came into force on July 1, 1987. The act was followed by work on what would become the Maastricht Treaty, which was agreed to on December 10, 1991, signed the following year, and came into force on November 1, 1993, establishing the European Union.

Establishment of the European Union

The European Union was formally established with the Maastricht Treaty, whose main architects were Helmut Kohl, the German chancellor (prime minister) and French president, François Mitterrand. The treaty established the three pillars of the European Union:

- the European Communities pillar—the European Community (EC), the ECSC, and the EURATOM, which handled economic, social, and economic policies;

- the Common Foreign and Security Policy (CFSP) pillar, which handled foreign policy and military matters;

- and the Justice and Home Affairs (JHA) pillar, which coordinated member states’ efforts in the fight against crime.

All three pillars were the extensions of existing policy structures. The European Community pillar was a continuation of the EEC. Additionally, coordination in foreign policy had taken place since the 1970s under the European Political Cooperation (EPC), first written into treaties by the Single European Act. While the JHA extended cooperation in law enforcement, criminal justice, asylum, and immigration, as well as judicial cooperation in civil matters; some of these areas were already subject to intergovernmental cooperation under the Schengen Implementation Convention of 1990.

The creation of the pillar system was the result of the desire by many member states to extend the EEC to the areas of foreign policy, military, criminal justice, and judicial cooperation. This desire was met with misgivings by some member states, most notably the United Kingdom, who thought some areas were too critical to their sovereignty to be managed by a supranational mechanism. The agreed compromise was that instead of completely renaming the European Economic Community as the European Union, the treaty would establish a legally separate European Union comprising the European Economic Community and entities overseeing intergovernmental policy areas such as foreign policy, military, criminal justice, and judicial cooperation. The structure greatly limited the powers of the European Commission, the European Parliament, and the European Court of Justice.

The European Union (EU) thus would emerge as a politico-economic union of 28 member states located primarily in Europe. The EU has developed an internal single market through a standardized system of laws that apply in all member states. EU policies aim to ensure the free movement of people, goods, services, and capital within the internal market, enact legislation in justice and home affairs, and maintain common policies on trade, agriculture, fisheries, and regional development. Within the Schengen Area, passport controls have been abolished.

The EU operates through a hybrid system of supranational and intergovernmental decision-making. The seven principal decision-making bodies—known as the institutions of the European Union—are the European Council, the Council of the European Union, the European Parliament, the European Commission, the Court of Justice of the European Union, the European Central Bank, and the European Court of Auditors.

Move to the Euro

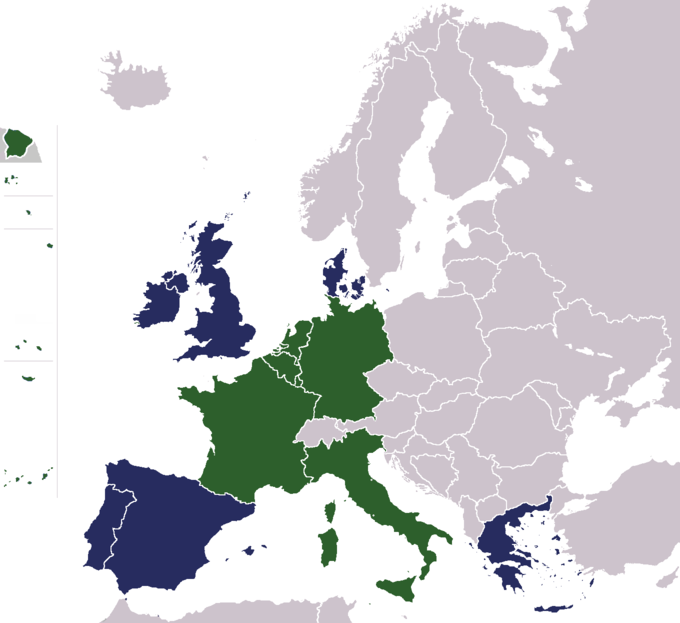

The eurozone is a monetary union of 19 of the 28 European Union member states that have adopted the euro as their common currency and sole legal tender to coordinate their economic policies and cooperation. A first attempt to create an economic and monetary union between the members of the European Economic Community (EEC) goes back to an initiative by the European Commission in 1969. The initiative proclaimed the need for “greater coordination of economic policies and monetary cooperation” and was introduced at a meeting of the European Council. The European Council tasked Pierre Werner, Prime Minister of Luxembourg, with finding a way to reduce currency exchange rate volatility. His report was published in 1970 and recommended centralization of the national macroeconomic policies, but he did not propose a single currency or central bank.

In 1971, U.S. President Richard Nixon removed the gold backing from the U.S. dollar, causing a collapse in the Bretton Woods system that affected all the world’s major currencies. The widespread currency floats and devaluations caused a set back for European monetary union aspirations. However, in 1979, the European Monetary System (EMS) was created, fixing exchange rates onto the European Currency Unit (ECU), an accounting currency introduced to stabilize exchange rates and counter inflation. In 1989, European leaders reached agreement on a currency union with the 1992 Maastricht Treaty. The treaty included the goal of creating a single currency by 1999, although without the participation of the United Kingdom. However, gaining approval for the treaty was a challenge. Germany was cautious about giving up its stable currency, France approved the treaty by a narrow margin, and Denmark refused to ratify until they got an opt-out from the planned monetary union (similar to that of the United Kingdom’s).

In 1994, the European Monetary Institute, the forerunner to the European Central Bank, was created. After much disagreement, in 1995 the name euro was adopted for the new currency (replacing the name ecu used for the previous accounting currency) and it was agreed that it would be launched on January 1, 1999.

In 1998, 11 initial countries were selected to participate in the initial launch. To adopt the new currency, member states had to meet strict criteria, including a budget deficit of less than 3% of their GDP, a debt ratio of less than 60% of GDP, low inflation, and interest rates close to the EU average. Greece failed to meet the criteria and was excluded from joining the monetary union in 1999. The UK and Denmark received the opt-outs, while Sweden joined the EU in 1995 after the Maastricht Treaty, which was too late to join the initial group of member-states.

In 1998, the European Central Bank succeeded the European Monetary Institute. The conversion rates between the 11 participating national currencies and the euro were then established.

Launch of the Eurozone

The currency was introduced in non-physical form (traveler’s checks, electronic transfers, banking, etc.) at midnight on January 1, 1999, when the national currencies of participating countries (the eurozone) ceased to exist independently in that their exchange rates were locked at fixed rates against each other, effectively making them mere non-decimal subdivisions of the euro. The notes and coins for the old currencies continued to be used as legal tender until new notes and coins were introduced on January 1, 2002. Beginning January 1, 1999, all bonds and other forms of government debt by eurozone states were denominated in euros.

In 2000, Denmark held a referendum on whether to abandon their opt-out from the euro. The referendum resulted in a decision to retain the Danish krone; this set back plans for a referendum in the UK as a result.

Greece joined the eurozone on January 1, 2001, one year before the physical euro coins and notes replaced the old national currencies in the eurozone.

The enlargement of the eurozone is an ongoing process within the EU. All member states, except Denmark and the United Kingdom which negotiated opt-outs from the provisions, were obliged to adopt the euro as their sole currency once they meet the criteria.

Following the EU enlargement by 10 new members in 2004, seven countries joined the eurozone: Slovenia (2007), Cyprus (2008), Malta (2008), Slovakia (2009), Estonia (2011), Latvia (2014), and Lithuania (2015). Seven remaining states remained on the enlargement agenda: Bulgaria, Croatia, Czech Republic, Hungary, Poland, Romania, and Sweden. Sweden, which joined the EU in 1995, turned down euro adoption in a 2003 referendum. Since then, the country has intentionally avoided fulfilling the adoption requirements.

Several European microstates outside the EU have adopted the euro as their currency. For the EU to sanction this adoption, a monetary agreement must be concluded. Prior to the launch of the euro, agreements were reached with Monaco, San Marino, and Vatican City by EU member states (Italy in the case of San Marino and Vatican City and France in the case of Monaco) allowing them to use the euro and mint a limited amount of euro coins (but not banknotes). All these states previously had monetary agreements to use yielded eurozone currencies. A similar agreement was negotiated with Andorra and came into force in 2012. Outside the EU, there are currently three French territories and a British territory that have agreements to use the euro as their currency. All other dependent territories of eurozone member states that have opted not to be a part of EU, usually with Overseas Country and Territory (OCT) status, use local currencies, often pegged to the euro or U.S. dollar.

Montenegro and Kosovo (non-EU members) have also used the euro since its launch, as they previously used the German mark rather than the Yugoslav dinar. Unlike the states above, however, they do not have a formal agreement with the EU to use the euro as their currency (unilateral use) and have never minted marks or euros. Instead, they depend on bills and coins already in circulation.

Technological and Social Change

Since the end of the World War II, advances in technology have also spurred global economic growth.

In the 1950s and 1960s the television was the technology device that most impacted the world economy. An American inventor, Philo Farnsworth fashioned together the first experimental TV in 1927, and the commercial manufacture of televisions began in the 1940s. By 1960, over 60 million TVs were sold in the United States alone. Radio networks such CBS and NBC established television stations, which featured variety shows and sporting events, as well as dramas and comedies. These networks financed these productions by selling commercial slots to companies who wanted to advertise their products to television audiences. Television thus enabled companies to promote and sell their products to a larger national and even international market. Television shows and advertising inspired consumers to purchase goods and spurred a consumer driven economy. For example, the 1956 appearance of Elvis Presley on The Ed Sullivan Show prompted millions of love-struck teenage girls to purchase the records of this musician and increased the profits of the recording industry.

The development of a network of satellites in space allowed events to be broadcast on television worldwide. The Soviet Union launched the first satellite, Sputnik into space in 1957. In the 1950s and 1960s during the Cold War, the Soviet Union and the United States engaged in a “space race,” a competition to explore outer space. One of the results of this Cold War competition was the development of the commercial use of space satellites to broadcast events around the world. Ironically the first live television broadcast using satellites was a performance of the song All You Need is Love by the musical group, the Beatles in 1967. Beginning in the 1980s consumers could access numerous television channels through electronic cables as well as through satellites.

The computer is another electronic device that has impacted the world economy especially since the 1980s. Computers had their origins in efforts to create electronic counting devices (i.e., cash registers) to expedite mathematical calculations. International Business Machines (IBM) in the 1920s emerged as a leader in this industry in the United States. John Maunchly and J. Presper Eckert invented the first computer in 1951 at the University of Pennsylvania. In the 1960s IBM emerged as the world's leading manufacturer of computers, which were large and bulky and owned by large businesses and governments. In 1977 Steve Jobs and Steve Wozniak unveiled the first Apple personal computer in the United States. Over the next several decades, personal computers (PCs) steadily increased their ability to store information and their speed in transmitting this information. PCs also became less bulky and expensive.

By 2007 consumers could transmit and receive information through a PC via the World Wide Web (the internet) or through a phone. The World Wide Web was invented by the English computer scientist Timothy John Berners-Lee in 1989. And in 2007 Steve Jobs introduced the first “smartphone” that combined the functions of a PC and a phone and could fit into a person's pocket or purse: the Apple iPhone.

The development of PCs and the World Wide Web has created a whole new industry, which is centered at “Silicon Valley” near San Francisco in the United States. This new industry has resulted in the creation of a host of new businesses and jobs.

Computers have also improved efficiency and productivity in the world economy since they facilitate the transmission of information. Some historians have maintained that computers have inaugurated a new “Information Age,” which will transform the world economy. Since the advent of the PC, much of the world has experienced unparalleled, extended periods of uninterrupted economic growth (1983 – 1990, 1991 – 2000, 2001 – 2007). Robotics and Artificial Intelligence (AI)—off-shoots of computer advancements—could impact society and the economy to the same extent as the introduction of the steam engine and the factory system in 18th century Europe. Since the computers are a relatively new development in human history, its historical impact is still unclear and to be determined over time.

World Trade Organization

Recent decades have also witnessed increased efforts around the world to expand and regulate international trade. The World Trade Organization (WTO) is an intergovernmental organization that regulates international trade. The WTO officially commenced on January 1, 1995, under the Marrakesh Agreement signed by 123 nations on April 15, 1994, replacing the General Agreement on Tariffs and Trade (GATT), which commenced in 1948.

The WTO deals with regulation of trade between participating countries by providing a framework for negotiating trade agreements and a dispute resolution process aimed at enforcing participants’ adherence to WTO agreements, which are signed by representatives of member governments and ratified by their legislatures. Most of the issues that the WTO focuses on derive from previous trade negotiations, especially from the Uruguay Round (1986 – 1994).

The WTO has attempted to complete negotiations on the Doha Development Round, which was launched in 2001 to lower trade barriers around the world with an explicit focus on facilitating the spread of global trade benefits to developing countries. There is conflict between developed countries—who desire free trade on industrial goods and services but retention of protectionism on farm subsidies for the agricultural sector—and developing countries—who desire fair trade on agricultural products. This impasse has made it impossible to launch new WTO negotiations beyond the Doha Development Round. As a result, there have been an increasing number of bilateral free trade agreements between governments. Adoption of the Bali Ministerial Declaration, which for the first time successfully addressed bureaucratic barriers to commerce, passed on December 7, 2013, advancing a small part of the Doha Round agenda.

Regional Integration

Another aspect of economic globalization involves regional integration, which is a process by which neighboring states enter into agreements to upgrade cooperation through common institutions and rules. The objectives of the agreement could range from economic to political to environmental, although it has typically taken the form of a political economy initiative where commercial interests are the focus for achieving broader sociopolitical and security objectives as defined by national governments. Regionalism contrasts with regionalization, which is, according to the New Regionalism Approach, the expression of increased commercial and human transactions in a defined geographical region. Regionalism refers to an intentional political process, typically led by governments with similar goals and values in pursuit of the overall development within a region. Regionalization, however, is simply the natural tendency to form regions, or the process of forming regions, due to similarities between states in a given geographical space

Regional integration has been organized either via supranational institutional structures, intergovernmental decision-making, or a combination of both.

Past efforts at regional integration have often focused on removing barriers to free trade within regions, increasing the free movement of people, labor, goods, and capital across national borders, reducing the possibility of regional armed conflict (for example, through confidence- and security-building measures), and adopting cohesive regional stances on policy issues, such as the environment, climate change, and immigration.

Since the 1980s, globalization has changed the international economic environment for regionalism. The renewed academic interest in regionalism, the emergence of new regional formations, and international trade agreements like the North American Free Trade Agreement (NAFTA) and the development of a European Union demonstrate the upgraded importance of regional political cooperation and economic competitiveness. In 1994, the United States, Canada, and Mexico signed NAFTA to lower or eliminate tariffs and create a large free trade zone incorporating the North American continent. The African Union was launched on July 9, 2002, and a proposal for a North American region was made in 2005 by the Council on Foreign Relations’ Independent Task Force on the Future of North America. In Latin America, however, the proposal to extend NAFTA into a Free Trade Area of the Americas that would stretch from Alaska to Argentina was ultimately rejected by nations such as Venezuela, Ecuador, and Bolivia. It has been superseded by the Union of South American Nations (UNASUR), which was constituted in 2008.

The Developing World

Although developing countries’ economies have tended to demonstrate higher growth rates than those of developed countries, they tend to lag behind in terms of social welfare targets.

Economic development originated as a global concern in the post-World War II period of reconstruction. In President Harry Truman’s 1949 presidential inaugural speech, the development of undeveloped areas was characterized as a priority for the West. The origins of this priority can be attributed to the need for reconstruction in the immediate aftermath of World War II, the legacy of colonialism in the context of the establishment of a number of free trade policies and a rapidly globalizing world, and the start of the Cold War with the desire of the U.S. and its allies to prevent satellite states from drifting towards communism. Changes in the developed world’s approach to international development were further necessitated by the gradual collapse of Western Europe’s empires over the following decades because newly independent ex-colonies no longer received support in return for their subordinate role to an imperial power.

The launch of the Marshall Plan was an important step in setting the agenda for international development, which was combining humanitarian goals with the creation of a political and economic bloc in Europe allied to the U.S. This agenda was given conceptual support during the 1950s in the form of modernization theory as espoused by Walt Rostow and other American economists.

By the late 1960s, dependency theory arose, analyzing the evolving relationship between the West and the Third World. Dependency theorists argue that poor countries have sometimes experienced economic growth with little or no economic development initiatives, such as in cases where they have functioned mainly as resource-providers to wealthy industrialized countries. As such, international development at its core has been geared towards colonies that gained independence with the understanding that newly independent states should be constructed so that the inhabitants enjoy freedom from poverty, hunger, and insecurity.

In the 1970s and early 1980s, the modernists at the World Bank and IMF adopted the neoliberal ideas of economists such as Milton Friedman or Bela Balassa. They implemented structural adjustment programs, while their opponents promoted various bottom-up approaches ranging from civil disobedience and critical consciousness to appropriate technology and participatory rural appraisal.

By the 1990s, some writers and academics felt an impasse had been reached within development theory, with some imagining a post-development era. The Cold War had ended, capitalism had become the dominant mode of social organization, and UN statistics showed that living standards around the world had improved significantly over the previous 40 years. Nevertheless, a large portion of the world’s population was still living in poverty, their governments were crippled by debt, and concerns about the environmental impact of globalization were rising. In response to the impasse, the rhetoric of development has since focused on the issue of poverty, with the concept of modernization replaced by shorter term visions embodied by the Millennium Development Goals and the Human Development approach, which measures human development in capabilities achieved. At the same time, some development agencies are exploring opportunities for public-private partnerships and promoting the idea of corporate social responsibility with the apparent aim of integrating international development with the process of economic globalization.

Critics have suggested that such integration has always been part of the underlying agenda of development. They argue that poverty can be equated with powerlessness, and that the way to overcome poverty is through emancipatory social movements and civil society, not paternalistic aid programs or corporate charity. This approach is embraced by organizations such as the Gamelan Council, which seeks to empower entrepreneurs through micro-finance initiatives, for example.

While some critics have been debating the end of development, however, others have predicted a development revival as part of the War on Terrorism. To date, however, there is limited evidence to support the notion that aid budgets are being used to counter Islamic fundamentalism in the same way that they were used 40 years ago to counter communism.