- Author:

- Tyler Schau

- Subject:

- Finance, Agriculture

- Material Type:

- Activity/Lab, Homework/Assignment, Reading

- Level:

- High School, Community College / Lower Division, College / Upper Division

- Tags:

- License:

- Creative Commons Attribution

- Language:

- English

- Media Formats:

- Text/HTML

Amortized Loan Labs

Line of Credit Example

Simple Interest - Line of Credit Lab

Simple Interest - Operating Loan Lab

Credit in Agriculture

Overview

This unit covers different types of loans that agricultural producers commonly use in the business of farming and ranching. It explains some key terms that are important to understand, and provides the equations and framework for setting up loans for short-term (operating loans and lines of credit) as well as amortized loans (equal principal payment loans and equal total payment loans).

Credit in Agriculture - Introduction

Understanding Capital and Credit in Agriculture

The term capital includes money invested in livestock, machinery, buildings, land and any other asset that is either purchased or sold. Agriculture has one of the highest per worker capital investment of any U.S. industry. The “capital” is what helps to make the U.S. farmer as productive as he/she is.

A discussion about credit is also important at this point, since many times when we need to purchase capital, we do not have the funds in order to do so. This is where credit comes into play. When you use credit to purchase an asset, whether that asset is a house, a car, a tractor or a bull, you use someone else’s money to purchase the asset and at the same time, make a promise to repay that person, generally with interest. Interest can be thought of as the cost of borrowing capital from someone else. Recall from your economics course the concept of “opportunity cost,” in this case when you borrow money from someone else, they no longer have access to those funds. In order to make it worthwhile for them to do without that “capital” right now, you will need to pay them for their opportunity cost of not getting to use their capital.

Let’s use a simple idea to start with. You are a college student and you don’t have a lot of money. You need to buy a car so that you can drive to your new job and earn money, but you don’t have any money, so it is difficult to buy a car. You find out that your roommate (who happens to have a car, and a job) has $2000 in a savings account, and you find a car that you would like to buy for $1500. You make your roommate a proposal, she loans you $1500 to buy the car, and in return you will pay back the $1500, plus an additional $200 in interest, by the end of 1 year (12 months). Your roommate thinks about it, currently the $2000 she has in her savings account is earning 0.50% APR (annual percentage rate). This means that her annual return on the $2000 is:

That is right, the opportunity cost for your roommate is only $10, which essentially means that by giving you the money in her savings account, she is only giving up $10. But remember you only need $1500 of her money, so really she will still be able to keep $500 in savings, so technically she will only be giving up $7.50. So why would you offer your roommate the $200 in interest payment? One word – RISK. Risk is a very abstract term, but the idea we want to convey here, is that risk means the chance that you might not pay back the money at all. What happens if you lose your job, get kicked out of school, and Mom and Dad disown you? How will you pay back your roommate? Since all of these are unknown and unanswered questions at the time of the transaction, the risk has to be priced into the interest payment. In this case if you calculate the interest rate on the loan that you offered to your roommate, you would find the rate to look something like this:

We can see now that you have offered to pay back your roommate an interest rate of 13.33% per year, but recall that her opportunity cost of capital was only 0.50%. This means that the risk that you represent is 12.83%. But remember that when her money was in the bank it was insured by the FDIC to be there, she had access to the cash whenever she needed it. Now that you are using it to purchase your car, that option is no longer available. And there is little or no guarantee that she will get paid back her principal or interest.

There are some tricks to reducing your risk and the risk of the lender (in this case your roommate). One way to reduce risk is security. Security simply put, means that if you “default” (are unable to pay back the loan) the lender will receive something of value, known as collateral. Most of the time the collateral will be the asset that is being purchased. Later we will discuss the times when the asset itself is not used as collateral, and the options that are available. But for now, let’s assume that you choose to use the $1500 car as collateral. Also assume that after a few weeks you lose your job because you don’t like to work very hard! While you sit at home and whine and complain, your roommate keeps going to work and class and does stellar. At the end of the year, you turn the keys and the title over to your roommate (actually if she was smart, she would have put the title in her name, since she is the one that paid for the car) and the car is now hers. There is a problem for her however. That car is NOT a $1500 car anymore because of a little thing we call depreciation. We will cover depreciation more in depth in a later class, but what is important for you here, is that assets have value (are worth money) because of what they can produce for us (say land that can grow corn, or a cow that can have calves, a combine that can harvest the corn, or a machine that can turn sheet metal into parts for the combine – a press break). They also have value based on what they can do for us (a vehicle used to transport you from your home to work, the house that you live in since it shields you from the weather, or your iPhone that lets you call people, check Snapchat and text messages). Since you have driven this car that you paid $1500 for several miles over the year, and possibly spilled your McDonalds on the floor, it is most likely worth less money than what you paid for it. So your roommate isn’t getting a $1500 car back, instead she is getting an $1100 car. In essence, since you weren’t able to pay the interest or the principal on the loan, your roommate took a $400 loss. This loss is often times referred to in business and economics as a “haircut”.

So how do lenders cover themselves from the risk of a loss when repayment does not occur and the asset has depreciated in value? Generally speaking a lender will require a down payment often referred to as “down” or “money down”. Think back to the original terms of the deal: you borrowed $1500 (principal) from your roommate, to buy a $1500 car (asset), the rate was 13.33% APR (Annual Percentage Rate), and the time was 1 year (meaning you would pay back the principal and interest accrued in 1 year). If you and your roommate were diligent about your deal, you would have placed all of the things on a document often referred to as a “term sheet” which is essentially a contract that spells out the details of a loan agreement between the borrower and the lender. Now if your roommate was confident that you would be able to pay off the loan they would write up the term sheet, you would keep your job and at the end of the year everyone would be happy. When it comes down to it, finance is a lot like a time machine. It allows you to pull resources from the future that you haven’t yet earned (wages from your job) into the present to purchase assets you need now (your car). In the same token it works the same for your roommate, only in reverse. She is able to send capital (the $1500 she lends you) that she has in the present into the future where it will be worth more (the original $1500 + the $200 in interest), so her $1500 she has now will be worth $1700 in a year. Bam - a time machine!

But what happens when you can’t pay off the “note” (another term for loan)? Well most sophisticated lenders have a plan for this, and it is the “down” that we talked about earlier. If your roommate would have made you spend $500 of your own money, she would have only needed to loan you an additional $1000, and would have received an interest payment of $133.33 along with the original $1000 at the end of the year if things went good. If they happened to go bad (as in our example) because you chose to play COD and Madden all damn night, your roommate would get your car, which is now worth $1100. Of course she will have the expense of getting rid of the piece of junk and the time invested in selling it, but at least when requiring you to put some money down, the lender is not losing on the bet.

Simply put, a bet is probably the best way to describe loans and finance. You are betting that you will be able to keep a job and earn enough income to pay back the loan, and your roommate (the lender) is betting the same. Over the years lenders have found ways to make their bets “safer.” In biblical times they could enslave borrowers that couldn’t repay debts! Loan sharks use the threat of violence to you and close friends and families to insure that debts get repaid! Actual above board lenders use things like down payments, security (collateral), term sheets, threat of credit score reductions, and even default insurance to make sure they are covered in the event of default (not getting paid back). But they are never fully protected. The lender is quite simply taking the risk of loss on for the borrower in exchange for a payout at the end.

Taking Credit to the Next Level

So we understand the need for credit and what it can do for us, but the roommate/car example was a little simplistic. How do we take that simple idea and roll it over to a farming operation that has thousands if not millions of dollars in equipment, land and buildings? First we need to look at the different sources of credit that we have access to:

Owner Equity

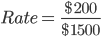

Any capital that you have already accumulated can be thought of as credit. Imagine you get out of college and get a job for the first ten years of your life. You spend very little of your money and save the rest. At the end of 10 years you decide to quit your job and start farming (or any other business you want to start). You now have $100,000 in a savings account. This money can be used to get you started in business by either using to purchase assets outright, or using it as a down payment on assets, so that you can use it as “leverage” to purchase even more assets. What is leverage you ask? Think of the teeter-totter from the playground where you grew up. A teeter-totter is a “leverage tool” and to have a leverage tool you need a few things, mainly a lever (the board that you sit on) and a fulcrum (the pivot point on the teeter-totter). See the image below:

So what do teeter-totters have to do with capital and credit? The idea is simple, think of credit as the “fulcrum”, the further to the right you place the fulcrum, the less work is needed to lift the object. So in other words, by using more of someone else’s money and less of your own “equity” you can purchase more things.

Take that $100,000 you have saved up in the bank. You could buy 1 $50,000 tractor and 20 acres of land for $2500/acre. But that doesn’t get you very far does it? But what if you put your equity to work as a down payment and borrowed the remainder from an outside source of credit. Say you put $10,000 down on the tractor, and $15,000 down on the land? You still have $75,000 left over in your account. You can put $25,000 down on a combine, $10,000 down on a seeder, and save the remaining $40,000 for operating expenses such as land rent, seed, chemical, fuel, fertilizer, etc. By borrowing money and using the capital/equity that you have access to you can “leverage” your way to having access to more assets, and more assets generate more returns.

Outside Equity:

Leasing

Leasing is an alternative that has sprung up in recent years. In essence you are simply renting the asset from someone else. Many of the top equipment manufacturers and dealers now have leasing options available. Leasing is much cheaper on a short-term basis than buying outright or taking on a debt. But with leasing you never gain any equity. This is the reason so many people are eager to buy houses after college. Why pay rent to someone, when you could pay a mortgage to the bank, all the while you will be increasing your equity every time you make a note payment.

For many farmers and ranchers that cash rent a lot of land, leasing makes good rational sense. For one the amount of acres (size of your business) can fluctuate year to year. Maybe you lose a few sections of land and no longer need a second or third tractor. With the lease option you can get out from under that payment rather quickly. Whereas if you borrowed money to buy that tractor, you would need to sell the tractor for enough money to cover the remaining debt on the note. This can be difficult and timely. In many cases producers that see varying levels of production every year many times will depend on the ability to lease equipment on a year by year basis. The annual cost will be higher, but you are not locked into the asset or the payment for a long period of time. This illustrates another concept of economics and finance – opportunity cost. All of the credit options we list here will have advantages and disadvantages. To gain in one area, there will be a cost associated with that gain.

Contracting

This is another method of credit that has increased in popularity over the last few decades. This time rather than buying an asset at all, you contract someone else to do the work for you. Examples of this are sending your calves to someone else to have them feed them out (custom feeding), I am able to retain the ownership of my calves and feed them to slaughter weight, but I do not have the expense of building a feedlot and purchasing all of the additional capital needed to feed cattle. Other examples are custom spraying, harvesting crews, finishing pigs on contract, etc. Typically, the operator provides the labor and management and some of the equipment or buildings. The operator will receive a fixed payment.

From the operator’s side (we are talking about operating the contracting business here, so say you do custom spraying) you are able to purchase an asset that might be of use on your operation, but you do not have enough work to pay for the asset itself on just your farm. So you contract your services out to other producers who might also be in the same boat as you. This helps them out since they will not also have to purchase a sprayer, but it also helps you out since it helps cover some of the cost of owning the asset.

Credit through Institutions

Borrowing money generally occurs through a financial intermediary such as a bank. Although at times they do come from other sources which we will look at later on. As we eluded to earlier borrowing money allows a business to “leverage” the capital that they already have. That can come in the form of using the capital as down payments on debts to purchase additional assets, or it can come in the form of acquiring additional capital (land, equipment, etc.) to compliment the capital that you already have. Borrowed money can provide a means to:

- Quickly increase business size.

- Improve the efficiency of other resources.

- Spread out the purchase cost of capital assets over time.

-Withstand temporary periods of negative cash flow.

Types of Loans

There are many ways to classify loans. Length of repayment, use of the funds and type of security pledged. All of them will include certain terms that are used in the credit industry, so it is important to understand what the terms mean and be familiar with them in order to communicate effectively with your lender.

Length of Repayment

Short-term Loans

Short-term loans are generally used to purchase inputs needed to operate through the current production cycle. Think fertilizer, chemical, fuel, wages to farm workers, etc. All of these items are things that must be purchased in order to do business, but sometimes we do not have the money to pay for them. Imagine you are just starting out farming for the first year, and have spent all of your money to pay for rent. How will you cover the cost of the inputs for your crop? Generally we call these short-term loans “operating loans”, because they mean precisely that – a loan to pay for the operating expenses. The reason that they are considered to be “short-term” is because once the crop is grown, harvested and sold, there should be enough money to available to pay back the loan. Since the typical harvest year for grains and livestock is one calendar year, the finance world has classified short-term loans to be loans that are paid back within 1 year, or less than 12 months.

Some businesses will instead set-up what are known as “lines of credit” which are basically a credit card with a lot lower interest rate. What the line of credit allows the business to do is to continue to write checks and purchase items such as fertilizer, feed, or any other input even though your bank account has $0 in it. So rather than having to go to the lender and ask for a loan to purchase inputs, the bank allows you to spend “credit” without their authorization. Much the same with a credit card, you will have a set spending limit or “credit limit” that you are allowed to borrow. By the way credit cards are also considered to be short-term loans as well.

Intermediate Loans

When a loan is repayable over more than 1 year, but less than 10 years it is classified as an “intermediate loan”. Often time’s banks refer to these types of loans as “chattel loans”. A chattel is a fancy word for property that is not fixed to real estate. Think of a tractor, it is a piece of property, but it can be moved (obviously since it has wheels). A mobile home is often classified as a chattel as well since it is well “mobile”. The advantage to an intermediate or a chattel loan is that since they are “movable” they can be sold much faster than a piece of “real estate” (land). Think back to the laws of economics and supply and demand for a brief second. The more buyers a market has, the higher the quantity demanded, and thus the higher the price. When “real estate” is for sale (think land, barns or stick built homes or items that cannot moved) the number of buyers in the market is much smaller. Only a handful of people are looking to buy farmland in Western North Dakota and most of them are already living in Western North Dakota. However, farmers all over the United States might be interested in your used 9660. Because of this, intermediate loans often carry a lower interest rate and banks often times require a smaller down payment. The risk of loss on the bet is much smaller for the lender.

Intermediate loans also carry the 1 – 10 year time frame because that is generally about how long they will last. Now obviously a tractor will last longer than 10 years. We all have or know someone that has an old Farm-all from 1950. But in business it is important to match up the length of repayment to the length of that assets “useful life”. For example I just bought a new truck in 2015. It has a 5 year note on it. By the time 5 years rolls around, that truck will have nearly 150,000 miles on it and will begin to suffer many break-downs and repairs. For the first 5 years it should have virtually no repairs besides basic maintenance. After 5 years, however, the repairs and maintenance will begin to occur and it would suck to be stuck paying a loan and repair bills. The same generally holds true for agricultural equipment and breeding livestock. It doesn’t make sense to be making debt payments and repair and maintenance payments at the same time. It also doesn’t make sense to borrow money on a bull to be paid off over 5 years, when his breeding life might only be 3 years. Matching up the length of the life of the asset on your operation to the length of the debt repayment is very important.

Long-Term Loans

A loan with a term of 10 years or longer is classified as a long-term loan. Assets with a long or indefinite life, such as land and buildings are often purchased with long-term loans. Land loans can be set up with a term of anywhere from 10 – 40 years. Long-term loans tend to carry higher interest rates since the risk on these assets is much higher than on an intermediate or a short-term loan. The risk is higher for 2 reasons; 1.) the time frame for bad things to happen is much longer and 2.) the asset is generally “not” mobile. Both of these cause the risk of the loan to be high, and the result of a high risk loan is a higher interest rate. Remember that not all loans will get paid back, so the loss on the loans that do not get paid back has to be absorbed by the money made on the loans that do get paid back.

Classifying by Security

The security for a loan refers to the assets pledged to the lender to ensure loan repayment. If the borrower is unable to make the necessary principal and interest payments on the loan, the lender has the legal right to take possession of the “mortgaged” assets. Mortgaged is another fancy term used in the finance world and it describes the process by which banks can file legal paperwork that entitles them to the asset should you be unable to pay back the loan. If default on a loan occurs, the lender can then sell the asset in order to recoup the cost of the loan. Assets pledged or mortgaged as security are called “collateral”.

Secured Loans

The term basically means what it says. The loan is backed by an asset of some sort. Generally the security is the asset that is purchased, sometimes it is another asset. Some financial institutions will have blanket or umbrella security which means they have an agreement with you that they can come take whatever they need in order to meet the value of the debt that you are unable to pay. This is the reasons that lenders like to visit farms and ranches. If they have loaned you money to buy 200 cows and a tractor, they want to make sure when they visit your place you have 200 cows and the tractor that they gave you money to purchase, rather than a snowmobile and a swimming pool for your kids. I know what you’re thinking “do people actually do that?” and the answer is YES. And by the way DO NOT DO THAT. If you borrow money from a lender for a specific asset, be sure to buy that asset and pay for it. You sign documents when you get the loan that are legally binding and if you purchase something else with that money, you have violated the contract you had with the bank which is illegal.

Unsecured Loans

A borrower with a good credit history of prompt loan repayment may be able to borrow some money with only a “promise to repay” or without pledging specific collateral. This is known as an “unsecured loan” or “signature loan”. Most banks prefer to not offer unsecured loans as there is no security. Most borrowers also do not prefer an unsecured loan because the interest rate will be much higher. Why? You guessed it, risk! When there is no recourse there is no incentive for me to repay the loan. They can’t take the asset or anything else they can only hurt my credit rating, so who cares? Now is a good time to talk about credit rating or credit scores.

If you have a credit card, you do actually have an unsecured loan. Think about the things you might buy with your credit card; gas, groceries, clothes, etc. These are things that either cannot be reused (as in the case with gas and groceries, once you use it to fuel either your car or your body it is gone) or the credit card company doesn’t want it back (like clothes, video games, etc.). That is why you have to sign your receipt when you buy something with your credit card, it is a “signature loan” remember. You are signing a document that says you will repay. There is where the term “credit” becomes really important and takes on a new meaning. Are you “creditworthy”? Which is basically the same thing as asking can I trust you? If the answer is yes, then a lender will be willing to extend credit to you. If the answer is no, then a lender will be less willing to lend you money as they do not think you will repay. Remember though that there is no way to accurately predict the outcome on everything in life, so lenders have these little tricks. One is the credit rating system, or your credit score. The following 3 pages help to explain the credit rating system and ways that you can keep in good standing in regards to your credit.

Simple Interest - Operating Loans

Simple Interest Loans in Agriculture

When we look at simple interest loans in agriculture, we are generally looking at paying for “operating expenses”. The fact that it is “simple” means that there is no compounding. The formula for simple interest as you may recall was:

So, what are operating expenses? It boils down to the fact that in business and on the farm, we have two types of expenses; fixed and operating. Fixed expenses are generally our large ticket items like tractors, buildings and land. We refer to them as fixed because we will use them this year, but we will also use them again next year and hopefully the year after that and so on. When we borrow money to purchase fixed assets, we will generally amortize those out (more on that in the next unit). Operating expenses, however, are the things that we need to purchase, but cannot use repeatedly. Things like fuel, seed, fertilizer, chemical and feed are all examples of operating expenses. If I want to grow a crop, every year I MUST buy more operating inputs. I do NOT have to buy a new tractor every year, but I DO need to buy more fuel every year to run it through the field.

We treat loans with respect to operating inputs differently than we do loans for fixed assets. The main reason has to do with the fact that the fixed assets will be in the business helping to generate revenue for several years and can be paid for using the revenue for several crop years. Operating expenses can only be used once though, so they need to be paid for in the year that they are used to produce a crop and thus revenue. Often-times though we will not have enough cash on hand to buy all the needed operating inputs; seed, chemical, fuel, fertilizer, land rent, and on and on. In that case we need to borrow the money from the bank in order to get the inputs purchased and in the ground. When we do this banks will offer a simple interest loan in two forms; 1st an operating loan or 2nd a line of credit.

For a lot of people these two ideas are interchangeable, but for now we will separate the two. An operating loan (or note as it is sometimes referred to) is a simple interest loan for a specific item, or a specific set of items. The operating loan will begin on a certain date for a set amount of money and will need to be repaid by a certain date or whenever the owner can pay off the loan. The classic example of the operating loan is for a cattle feeder. Cattle feeding is a very high operating cost business. You must purchase the calves that you are feeding as well as the feed and the labor every single crop year. As a result, cattle feeders will often have an operating loan for the cattle that they are feeding.

Lines of credit are slightly more complex than operating loans. Think of a line of credit like a series of several operating notes. On the average farm in North Dakota we will farm about 2000 acres and own about 75 cows. If our average operating cost per care is $175/acre and our average operating cost per cow is about $150 per cow, you are looking at nearly $361,250 per year in just operating expenses. If we took out an operating loan for each specific item that we were borrowing money for, that would be a lot of paperwork for both the owner and the banker. So, banks developed the idea of the line of credit, that basically says, you can borrow so much money every single year from the bank. The bank really doesn’t care what it is being spent on (it does, but it doesn’t make you call in as long as you have a good relationship with the bank) as long as you are able to pay back the loans at the end of the year. The best way to think of a line of credit is like a series of operating loans wrapped up into one note that tracks what you have spent, when and what you owe. Our job in these sections is to figure out how to calculate that amount.

Operating Loans (Operating Notes) – Calculations:

There are a few terms that you need to familiarize yourself with when it comes to operating loans. Principal is the amount that you borrow from the bank. Don’t’ confuse that with purchase price, which is what you pay for the asset. If you recall from Credit in Agriculture, banks will require a down payment in certain scenarios. That is why the principal and the purchase price will not always be the same. It also may be the case that we do not need to borrow the full amount for the operating loan. So, we pay what we can out of pocket and borrow the remainder.

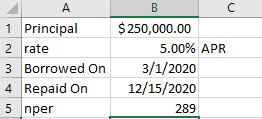

Example #1:

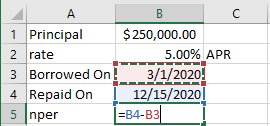

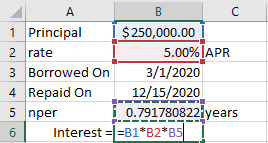

Assume that you are a farmer in 2020 and need to borrow money so that you can purchase seed, chemical, fertilizer and land rent for the upcoming crop season. On March 1st, you go to your lender and ask to borrow $250,000 for operating inputs. The bank gives you the loan and they put $250,000 into your checking account. You can use the money as you need it for what you need to purchase. The terms of the loan are that it is payable as soon as you are able, or by December 31st at the latest, the interest is set at 5.00% APR. Let’s also assume that you harvest your crop and sell most of it by December 15th, and free up enough cash to pay off the operating loan and the interest that has accrued so far. Let’s use excel to help us calculate the interest charges.

The first step in excel is to set-up a table and label things, then we will use excel to do the calculations for us:

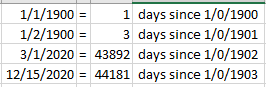

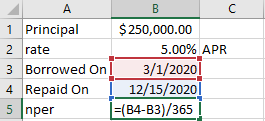

Notice in the screenshot above that we need to calculate how long the money is borrowed, rather than trying to count months, or weeks or days on your hands and feet, let excel do the work for you. So long as you use the correct format for the date, excel can do a simple subtraction problem to determine the number of days between the two dates. I like to enter in the date I borrowed the money as well as the date that I repaid the loan. Then I can enter a simple subtraction formula to get the nper (time period) of the loan – 289 days in this case. The reason this works is because excel converts the date to a number. 1/1/1900 is equal to 1, 1/2/1900 is equal to 2, etc.:

Because the days since 1/0/1900 is what excel is using for the value behind the scenes, you can use that trick to calculate the number of days in a lot of cases – a very handy trick in a lot of applications!

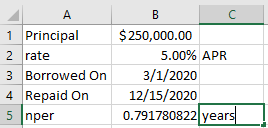

Back to the operating loan problem though. Now all we need to do is convert the nper into the same unit of time as the rate. Since the rate is an APR, it is annual units. To convert 289 days into years, I need to divide the number of days by 365 days/year. This conversion will give me the amount of years that I have the money borrowed:

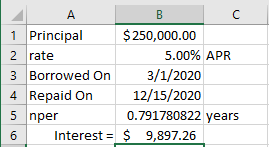

Now that I have that conversion done, it is a simple interest problem:

Thus:

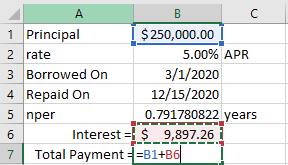

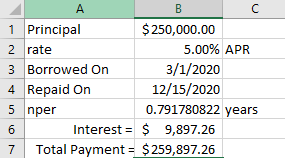

So the interest on $250,000 dollars borrowed on 3/1/2020 for 289 days at 5% APR is $9,897.26. But you will need to make a payment to the bank for both the principal borrowed and the interest. That payment is known as a total payment and it is the only time that the interest and principal get added together. This is an important detail to understand. Other than when we calculate the total payment, we never combine principal and interest. If you can remember that detail, your life will be much simpler. To get the total payment, all we need to do is add together the Interest and the Principal:

Here are a handful of operating loan problems to work on before we add a few more details to the mix:

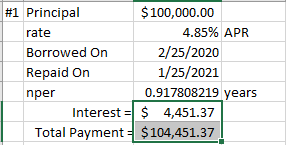

- A farmer borrows $100,000 on 2/25/2020 for inputs at 4.85% APR. He is able to pay off the loan on 1/25/2021. What is the interest due and the total payment made to the bank for the loan?

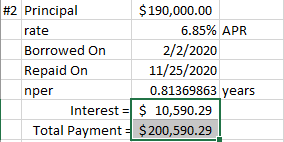

- A farmer borrows $190,000 on 2/2/2020 for inputs at 6.85% APR. He is able to pay off the loan on 11/25/2020. What is the interest due and the total payment made to the bank for the loan?

Most of the time farmers won’t utilize the operating loan for farm inputs. The reason is when I borrow the lump sum of money - $190,000 on 2/2/2020 as in problem #2 – I am now paying interest on the full $190,000 starting on 2/2/2020, even though I may not need some or a lot of that money until May or even June/July. I am basically paying interest to have money in my checking account, which doesn’t make a lot of sense, and that is why we will typically use lines of credit or these situations. One situation where we do use the operating loan, however, is in a cattle feedlot, where I have to pay a lot of money to buy the calves to put on feed. We cover these for several reasons; 1) some of you will buy cattle to feed in the future, 2) we can start adding in the concept of a down payment and 3) math problems in converting lbs. to cwt!

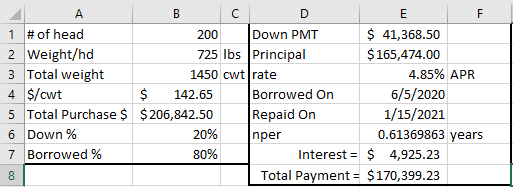

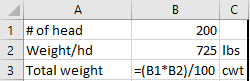

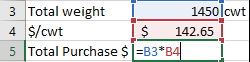

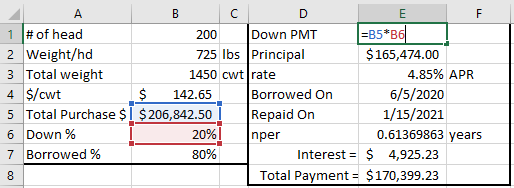

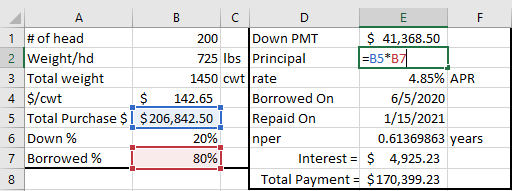

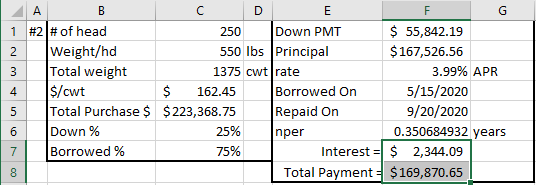

So, let’s assume that on 6/5/2020 you purchase 200 head of 725 lb. steers and pay $142.65/cwt for them. The bank loans you 80% of the money and charges you 4.85% APR interest. You feed the cattle to 1500 lbs. and sell them on 1/15/2021 and can pay off the loan to the bank. How much do we pay in interest? What is our total payment?

A few things that I should point out are the conversions that we do. The first is the conversion of pounds into cwt. Since we pay by the cwt, we need to know how many total cwt’s were purchased:

Then we can multiply the total weight purchased by the price per cwt:

The down payment and the principal borrowed will always add up to the value of the purchase price, so we can convert them from a percentage to a dollar value:

Once we have the principal, the rest is just like the problem before. Convert the dates to a year and then use the simple interest formula to calculate the interest and then add the interest to the principal to get the total payment (Dd not add the interest to the purchase price, we are calculating what we owe to the bank, if you did NOT borrow the full purchase price, you do NOT need to pay them back the full purchase price).

Here are a handful of operating loan problems to work on before we move onto Line of Credit problems:

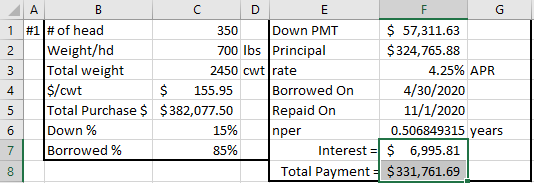

- On 4/30/2020 a cattle feeder buys 350 head of 700 lb. steers for $155.95/cwt. The bank loans him 85% of the purchase price at an APR of 4.25%. If the feeder sells the cattle on 11/1/2020 and is able to pay off the loan, what is the interest due and the total payment made to the bank for the loan?

- On 5/15/2020 a cattle backgrounder (runs calves on grass) buys 250 head of 550 lb. calves for $162.45/cwt. The bank loans her 75% of the purchase price at an APR of 3.99%. If she sells the cattle on 9/20/2020 and is able to pay off the loan, what is the interest due and the total payment made to the bank for the loan?

Simple Interest - Lines of Credit

Simple Interest Loans in Agriculture

To recap: The formula for simple interest as you may recall was:

Remember that we said one of the problems with using operating loans for operating inputs is that you had to start paying interest on the money as soon as you borrowed it. So, if you didn’t spend the money for another month or two, you were paying interest just have money in your account. In a business that can be as brutal as farming and ranching, managing interest costs can be the difference in success and failure. Luckily, you do NOT have to borrow all of your operating needs at one time. Most lenders will allow you to borrow money as it is needed. This is known as a line of credit. In essence the line of credit is a lot like a credit card. Albeit it works different with different banking institutions. Some require that you call the bank when you buy something, others just cover it, that will depend on who you are banking with. Either way, the process is pretty much the same, you write checks for the items that you need for operating expenses; seed, chemical, fertilizer, etc. and the bank makes sure that there is money in your account to cover the cost of those expenses. If your account balance is $0, the bank will pay for the item and add it to your line of credit. Operations have to apply for a line of credit, and as long as you haven’t “maxed out” your credit line.

*** Students hate doing line of credit problems. The math is simple (see Simple Interest formula above). The organization is the part that the students generally don’t like. You have to be able to organize data and use it to your advantage. The simple truth is that these are pretty easy, and take very little effort, so long as you are organized and can think in a table format.

Line of Credit – Calculations:

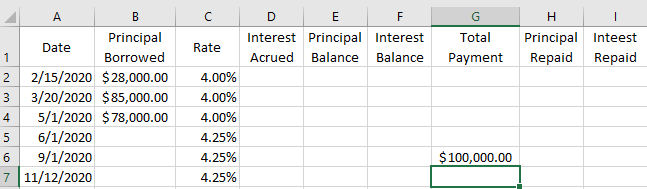

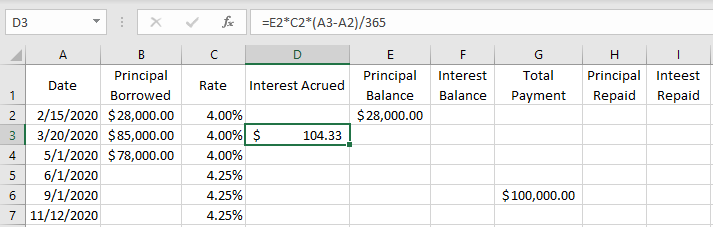

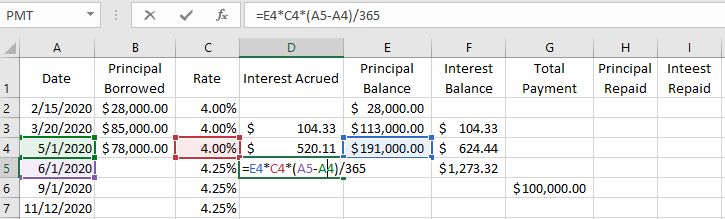

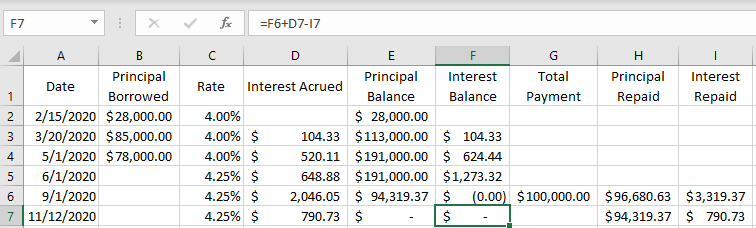

To start with we will keep this relatively simple. Let’s say we just need to purchase just three things on our line of credit, and we buy them together. So, on 2/15/2020 I am able to buy all of my fuel for the upcoming year. I purchase 20,000 gallons at $1.40/gallon for a total of $28,000. I put it on my line of credit, because I have no cash left and I do NOT want to sell any crop in the bin. The bank is currently charging me 4% APR on the line of credit. Then on 3/20/2020 I purchase all of my seed for the year and the total is $85,000, all of that goes on my line of credit as well. On 5/1/2020 I get the bill for all of my fertilizer and chemical for the year and that total is $78,000. On 6/1/2020 I get a notice that the interest rate on my line of credit will be going to 4.25% APR. On 9/1/2020 I am able to sell off some wheat and free up $100,000 that I use to pay down my line of credit. On 11/12/2020 I sell more crop and am able to pay off the line of credit completely. The two things that I need to know are how much interest do I end up paying in total and what is my total payment to the bank. But there are a lot of steps that I need to remember. The first is to create a table that helps me organize all of the information:

There are a lot of columns there, so let’s go through them quickly. The first few are pretty self-explanatory. You list the date that something changes (that term will be important – “when something changes”), so you can see that on 2/15/2020 we borrowed $28,000 against our line of credit, something changed in that we borrowed money so we enter the information. The principal borrowed is typed in if we borrowed money on that date. The interest rate as of that date is also entered into the rate column. Go through all of the things that happen during the duration of the line of credit problem and enter them into the table. Notice on 6/1/2020 the interest rate changes, so we make a note of it. On 9/1/2020 we make a payment against our line of credit, so we make a note of it and enter the information into the table. We only ever enter the information that we have, since I do not know how much of that $100,000 went to principal or interest right now, I leave it blank! The last entry is on 11/12/2020, that is entered because that is the day we are able to pay off the line of credit. We have to do a lot of problem solving to figure out how much we will pay off first though, that is why all we have done is listed the date and the rate.

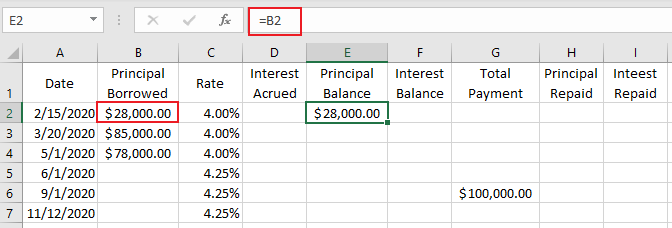

The next step is to start tracking our balances. Balances are accumulations. As I add more principal borrowed, my principal balance will start to increase by the additional amount borrowed. For the first line, the only thing that I can do is update my principal balance:

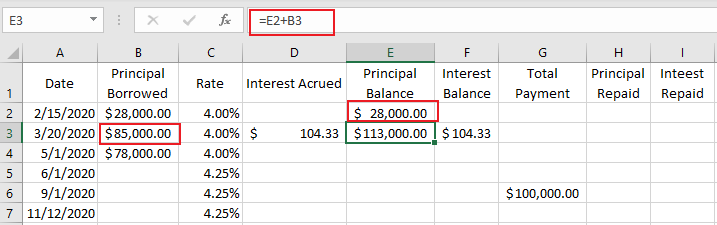

This brings me to rule #1 – you do nothing until something changes. So think about these as a time problem: on 2/15/2020 we borrow $28,000, our principal balance is now $28,000, and that is all we can do until something changes. Something changes on 3/20/2020 – we borrow an additional $85,000.

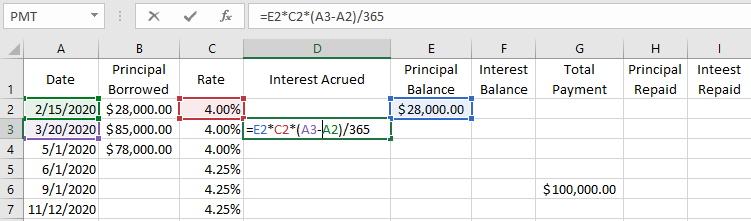

This brings us to rule #2 – when something changes, calculate the interest accrued up to that point first. It is still a simple interest problem, so we need to take $28,000 * 4% * 34/365, the reason we take 34/365 is because there are 34 days between 2/15/2020 and 3/20/2020 and since the rate is quoted in APR, the nper needs to be in the same unit as well, and there are 365 days in a year!

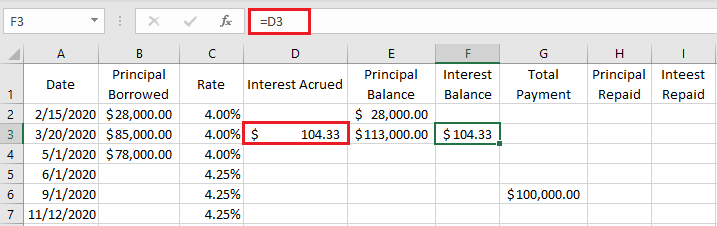

Rule #3 – after the interest up to that date has been calculated – update balances. That means that the interest accrued as of 3/20/2020 is $104.33. In other words, having borrowed the $28,000 on 2/15/2020 at 4% so far as 3/20/2020 we have accrued $104.33 in interest charges. Now that we have an interest calculated as of 3/20/2020 we can update our principal and interest balances.

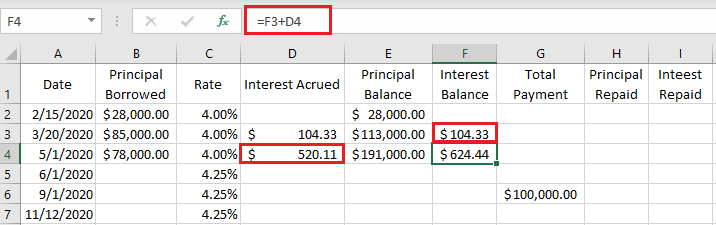

Rule #4 – Once the balances are updated revert back to rule #1, which is do nothing until something changes. Nothing changes until 5/1/2020 when we borrow another $78,000. At that time, we follow rules #2 and #3. We calculate interest up to that point and then we update our balances:

If we build the formulas correctly for calculating the interest accrued, we should be able to copy the formulas down and we will get the correct answers. The only formula that needs changed this time is the Interest Balance column since before it was just equal to the interest accrued. Now it is equal to the interest balance from the time period before plus the new interest accrued. Now we follow rule #4 and revert back to rule #1 – do nothing until something changes. Something changes on 6/1/2020, the interest rate adjusts higher to 4.25%. That means all dollars borrowed from that date on will accrue interest at the 4.25% rate:

Do take note that we are still using the 4.00% APR when calculating the interest as of 6/1/2020, that is because the rate doesn’t change until 6/1/2020, so all money borrowed up to that point accrues at the 4% rate.

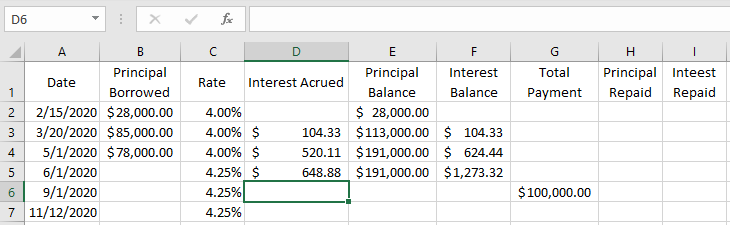

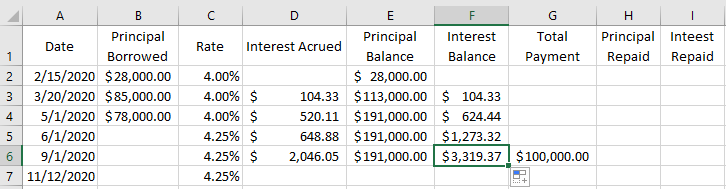

Now we go back to rule #1 and do nothing until 9/1/2020, when something changes when we make a payment against the line of credit. This introduces us to Rule #5 – When making a payment always pay the interest first. This is because that is the bank makes money, so that is what they want to get paid first. Our first job though is to calculate the interest through 9/1/2020, then we update our balances, then we make our payments and update our balances again:

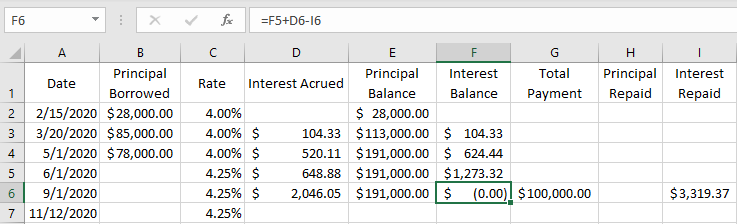

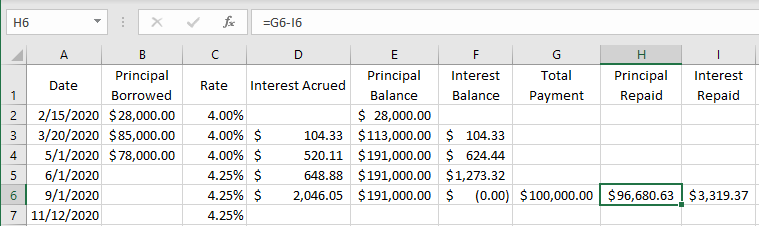

Since on 9/1/2020 our interest balance is $3,319.37, we will make an interest payment of $3,319.37, and since we are paying that off, we are introduced to Rule #6 – after making payments, update balances – Principal and Interest. Our interest balance will drop to $0 as a result:

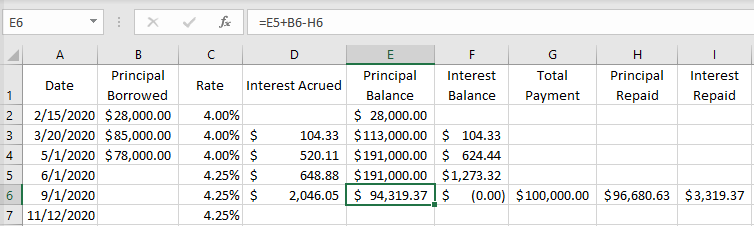

Now that we have calculated our interest payment, we can calculate our principal payment. Remember that total payments are the combination of principal and interest payments, so we take $100,000 - $3,319.37 = $96,680.63:

Since we made a payment against the principal, we have to update our principal balance. Principal balance is how we calculate the interest accrued. Since we have paid off some principal, we want to make sure that we reduce our principal balance so that the interest is calculating correctly:

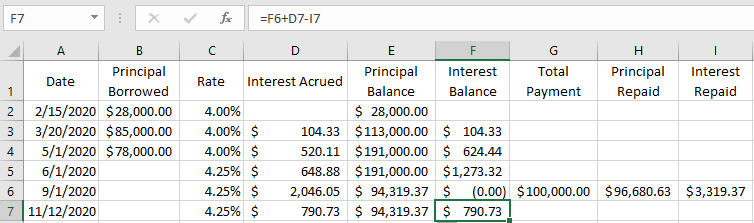

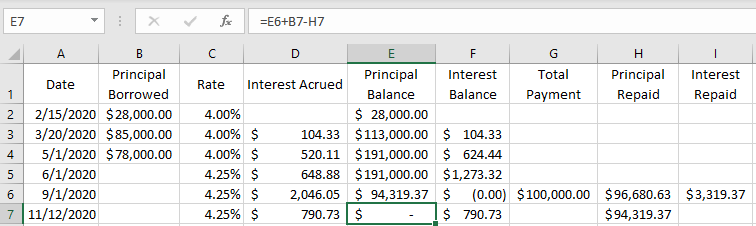

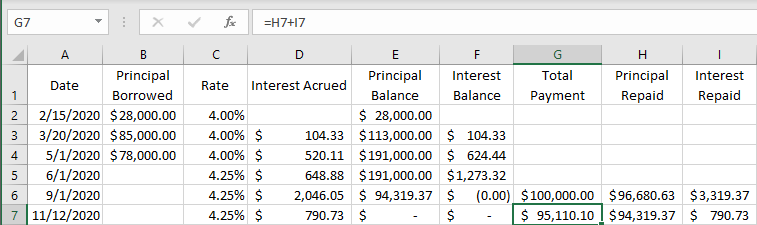

Now we can wrap it up, by calculating the interest accrued through 11/12/2020 and figuring out how much we will need to pay the bank to pay off the interest and the principal:

Since we still owe $94,319.37, we will need to pay that much in principal – “principal repaid”:

We also owe $790.73 in interest, so we need to pay that much in interest – “Interest Repaid”:

The last part is to calculate what your total payment made to the bank on 11/12/2020 is by adding the Principal Repaid and the Interest Repaid on 11/12/2020:

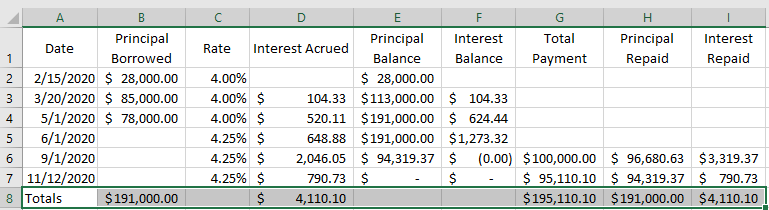

Rule #7 is to come up with totals:

The total for Principal Borrowed should be equal to the total for Principal Repaid. The total for Interest Accrued should be equal to the total for Interest Repaid. If they are there is a good chance that you have calculated things correctly!

Again, there are a lot of steps involved in correctly calculating lines of credit. And to be honest, the bank will do a much better job! So why are we learning to work through them? You will gain a lot of skills when it comes to organization of tables and thinking through problems. You will also better understand how your personal credit card works and accrues interest.

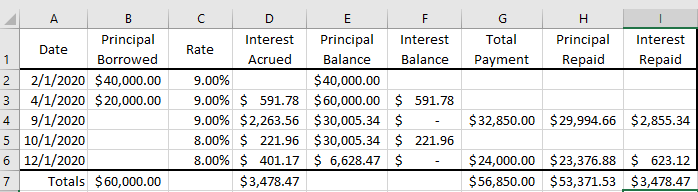

Here is another problem to work through; sometimes instead of writing out the problems in paragraph form, I will list them in a table:

| Date | Principal Borrowed | Rate | Total Payment |

| 2/1/2020 | $40,000 | 9% | |

| 4/1/2020 | $20,000 | 9% | |

| 9/1/2020 | 9% | $32,850 | |

| 10/1/2020 | 8% | ||

| 12/1/2020 | 8% | $24,000 |

One place where a lot of students get hung up on these, is the difference between the table that I gave you the information on, and the table that we need to calculate the answers. The table with the information, only contains the information needed to calculate the line of credit. But we need to know other things. That is why I often refer students back to the rules:

#1 - you do nothing until something changes.

#2 - when something changes, calculate the interest accrued up to that point first.

#3 - after the interest up to that date has been calculated – update balances – Principal and Interest.

#4 - once the balances are updated revert back to rule #1, which is do nothing until something changes.

#5 - When making a payment always pay the interest first.

#6 – After making payments, update balances – Principal and Interest.

#7 – After balances are adjusted and the table is completed, find totals for Principal Borrowed, Interest Accrued, Total Payment, Principal Repaid and Interest Repaid.

Amortized Loans

Amortized Loans

In the Introduction to this unit – “Credit in Agriculture” we talked about the difference between short-term and intermediate/long-term loans. In the previous two sections covering operating loans and lines of credit we looked at how we borrow money for and pay back loans for “operating inputs” items that get used once. In the following two sections we will look at how we borrow money for and pay back loans for assets that have a lifespan longer than 1-year in business. These are assets like tractors, land, and cows. These assets get used to produce a crop or calves in several different years. Therefore, it is not as important to pay for the asset in one year. We “amortize” or spread out the payment over the course of several years. Even if you never farm or borrow money to pay for land, or a tractor, there is a good chance at some point in life you will borrow money to buy a vehicle or a house, both of which will get amortized out over several years.

There are two methods for calculating amortized loans – Equal Principal Payment and Equal Total Payment. Equal principal payment loans mean exactly what they say you make equal payments of principal to the bank each time you make a payment (when you make payments to the bank, remember that you are paying them for both principal and interest). Equal total payments mean that when you make a payment to the bank, each installment or payment will be equal, meaning the amounts of principal and interest will change each payment, but the total will be the same. For this unit, we ware going to focus on Equal Principal Payments.

Equal Principal Payments:

Calculating the payments on an equal principal payment loan is actually fairly simple. Again, we use the simple interest formula:

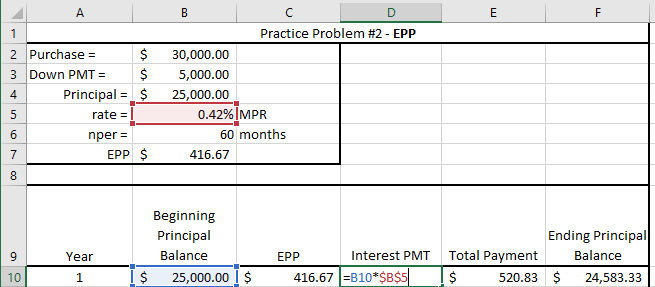

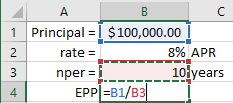

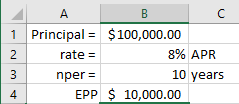

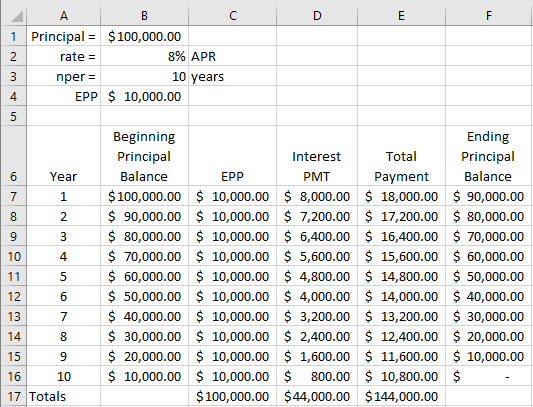

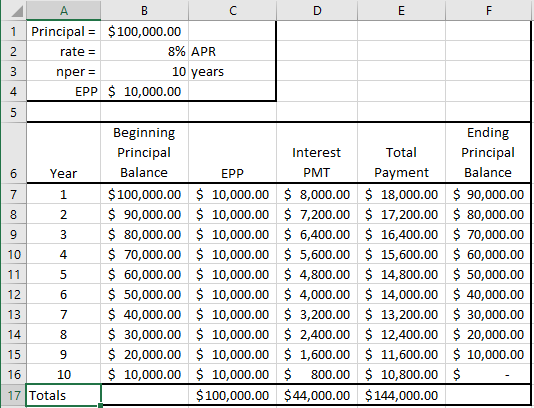

Example #1: The terms of the loan will dictate how the loan pay-off is calculated. For this example, we’ll use a $100,000 principal loan, 8% APR for 10 years making annual payments. Since this is an equal principal payment loan, it means that every time we make a payment, the amount of principal paid to the bank will be the same. That is pretty easy – we are making 1 payment each year, for 10 years. The calculation for the equal principal payment (EPP) is the principal divided by the number of payments; $100,000/10 pmts = $10,000 per payment. The rest of the problem is again a problem in organization and data management. Again, tables come in very handy, and so we need to use excel.

The key is setting up the table so that we have all of the information that is needed listed. See the screenshot below to see the proper method for setting up an amortization table for an equal principal payment loan:

Now we can set-up the amortization table:

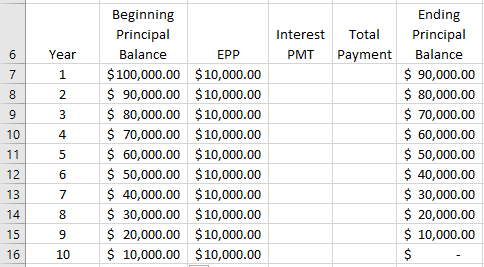

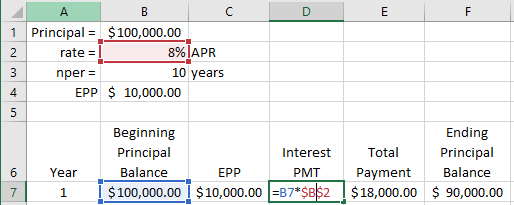

The beginning principal balance and ending principal balance and equal principal payment columns can be filled out immediately because we have that information. Remember that principal and interest balances must be segregated, meaning we do NOT combine them. The ONLY TIME principal and interest is combined is when we make a payment to the bank - “total payment”. That means the only thing left to do to finish this problem is to calculate the interest due each year, as well as the total payment. Remember that the calculation for interest is still just a simple interest problem. So all we need to do is multiply the beginning principal balance for that year times the interest rate times the nper (which in this case is 1 year, so that is a really simple calculation).

Interest PMT for Year 1 = $100,000 * 8% APR * 1 year = $8000

Total Payment for Year 1 = $10,000 (principal pmt) + $8,000 (interest pmt) = $18,000:

There are some simple tricks to use in excel to make life easier. The first is using cell referencing so that excel will automatically calculate the formulas that you build into the spreadsheet. The second is absolute positioning so that we can create formulas with the capability of click and drag copying. Below is the formula that I created to calculate interest PMT above:

By creating the table as we did above it becomes really easy to fill in the entire table:

The last step is to calculate the totals for the EPP column, the Interest PMT column and the Total Payment Column. These totals tell us the amount of money that we repaid the bank; total principal repaid = $100,000, total interest paid = $44,000 and total payment = $144,000.

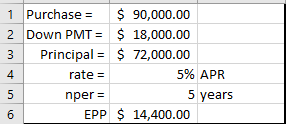

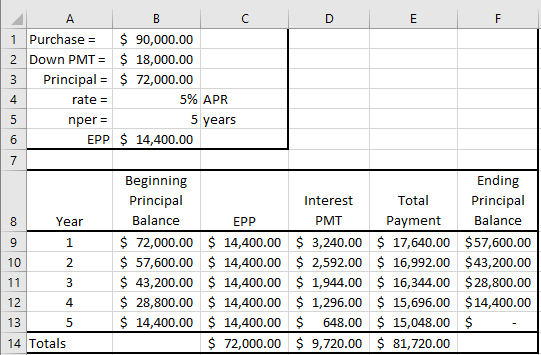

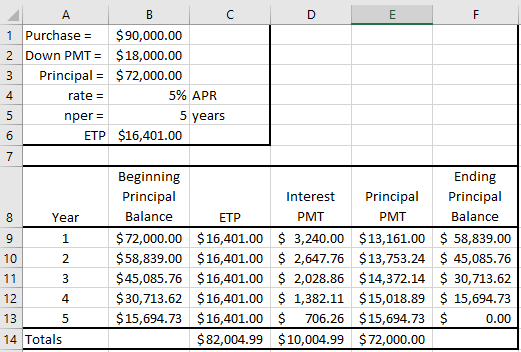

Example 2: You purchase a set of 50 heifers at $1800 per head. The bank loans you the money, at 4.50% APR. Terms of the loan are as follows; 20% down payment required, 5 years, annual payments, making EPP. Calculate the amortization table and answer the following questions: 1) What will be the total interest paid to the bank over the course of the 5 years? 2) What will be the total payment paid to the bank at the end of 5 years?

To break down the problem above, we must first figure out how much money will be borrowed from the bank – the principal. We are buying 50 head at $1800, so the total purchase price is $90,000. The bank is going to require a down payment of 20%, so we while have to cover $18,000 of the purchase price, which means that the principal will be $72,000. We are making annual payments for 5 years, so the EPP will be $14,400:

Equal Total Payments:

The second method of amortizing loans is Equal Total Payments (ETP). Again, this method does exactly what it says, it creates a payment plan where the total payment (principal plus interest) made to the bank is equal each payment. These loans are slightly more complex, but still revolve around the same table format as EPP loans. There is one extra step – but good thing for you, you learned it in an earlier unit – PMT formula. For these examples we will use the same examples as we used in the EPP calculations.

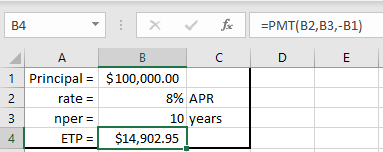

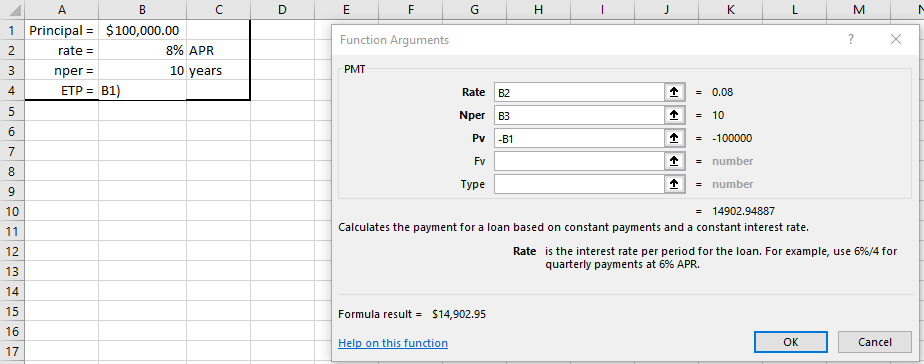

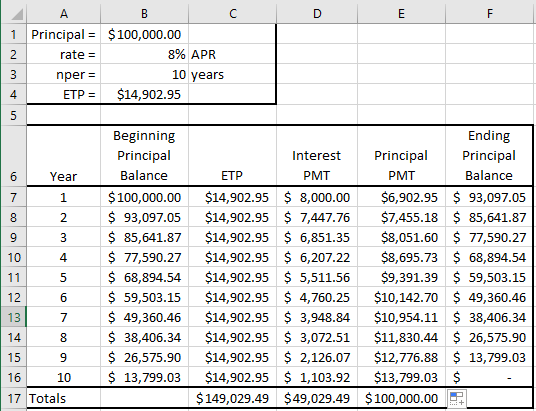

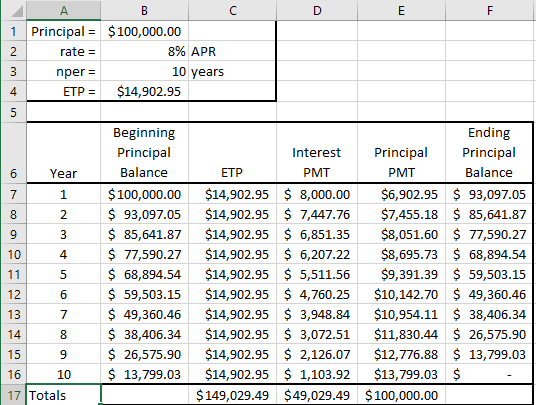

Example #1: The terms of the loan will dictate how the loan pay-off is calculated. For this example, we’ll use a $100,000 principal loan, 8% APR for 10 years making annual payments. Since this is an equal total payment loan, it means that every time we make a payment, the total amount paid to the bank will be the same. To calculate this, we need to use the PMT formula in excel:

See the screenshot below of the Function Arguments:

By using the PMT formula and plugging in the Rate, Nper and the PV (the principal is the PV since it is the amount we are borrowing right now) and leaving the FV blank and omitting Type since the payment is made at the end of year, we are given the ETP for this loan. Now all we need to do is build our table again, for the most part it is similar to the EPP table, but it makes more sense to move a few columns around:

The reason for rearranging the columns is to place what we can calculate in the first columns. We can calculate the ETP using the PMT formula. We can also calculate the interest. It is still a simple interest problem just like before, that is why the interest pmt in the first year for both EPP and ETP is $8000. If you think about it, it makes sense. In both loans, we have $100,000 borrowed for one full year at 8% APR. It doesn’t matter how it is paid back; we still owe $8000 in interest in year 1. Once we have the interest pmt calculated, we can use it to derive the principal pmt. Since the total pmt = interest pmt + principal pmt, the principal pmt = total pmt – interest pmt:

From there we simply fill in the cells to get the finished table.

Let’s compare the two types of loans EPP and ETP:

Which method casues the borrower to pay more in interest?

ETP creates a higher interest payment over the life of the loan.

Why?

Because we pay off the principal slower, which means there is more principal sitting out there accruing interest each year.

Which method is better?

It depends. EPP creates less interest expense for the borrower, but it does create higher payments in the first 5 years of the loan. Often borrowers will utilize ETP because of this. We already have to borrow money becuae we don’t have enough. We may be willing to pay more over the life of the loan in order to redcue payments early on.

Example 2: You purchase a set of 50 heifers at $1800 per head. The bank loans you the money, at 4.50% APR. Terms of the loan are as follows; 20% down payment required, 5 years, annual payments, making ETP. Calculate the amortization table and answer the following questions: 1) What will be the total interest paid to the bank over the course of the 5 years? 2) What will be the total payment paid to the bank at the end of 5 years?

Practice Problems:

- Purchase a tractor for $150,000. Bank requires a 25% down payment. Finances the remainder for 6.25% APR for 6 years, annual payments. Create an amortization table with totals for both the EPP and the ETP method.

- Purchase 500 acres of land for $1350/acre. The bank requires a 15% down payment. Finances the remainder for 4.80% APR for 20 years, annual payments. Create an amortization table with totals for both the EPP and the ETP method.

- Purchase 75 head of 3-year old bred cows for $1600/hd. The bank requires a 30% down payment and finances the remainder for 3.85% APR for 4 years, annual payments. Create an amortization table with totals for both the EPP and the ETP method.

See excel file – Amortized Loan Examples for the answers.

What about monthly payments? Again, as we have covered thus far, the interest rate and the time always need to be in the same unit. So, what happens when you make monthly payments? If the interest rate is quoted as an APR, the rate needs to be converted to a monthly rate. The simple rule of thumb is that the rate needs to match up with the payment method. If it is annual payments, the rate is quoted as an APR. If it is monthly payments, the rate needs to be quoted as an MPR. A quick example:

- You purchase a car for $30,000 and make a $5,000 down payment. The bank finances the remaining $25,000 for 5 years, monthly payments at an APR of 5%. Create an amortization table with totals for both the EPP and the ETP method.

See excel file – Amortized Loan Examples for the answers.

The table is pretty long, so it doesn’t make sense to add the screenshot here. What you will notice is that there are now 60 payments (5 years * 12 months/year). Also, when you calculate the interest payment the formula, the time (nper) is still one. Since you adjusted your rate to monthly, the time period is calculating interest for one month: