- Author:

- La Tasha Roberts

- Subject:

- Accounting

- Material Type:

- Reading

- Level:

- Community College / Lower Division

- Tags:

- License:

- Creative Commons Attribution

- Language:

- English

Financial Accounting Classify Accounts

https://quickbooks.intuit.com/accounting/cash-vs-accrual-accounting-whats-best-small-business/

https://www.basis365.com/blog/cash-basis-accounting-and-accrual-accounting

https://www.investopedia.com/terms/a/accounts-receivable-aging.asp

https://www.sos.state.tx.us/corp/businessstructure.shtml

OER_ch01 Student

Accounting For Business and Entrepreneurs, Concepts and Technology

Overview

The content will cover basic Accounting and Managerial concepts for Non-Accounting Majors. This textbook approaches Financial and Managerial Accounting from a business perspective. The topics covered are relevant for business owners and entrepreneurs; helping them to understand what information is needed to run a business, make decisions, and grow the business.

Table of Contents

Chapter 1: Introduction to Accounting

Chapter 2: Analyzing, Posting, and Adjusting Transactions

Chapter 3: Receivables

Chapter 4: Accounting for a Merchandising Company

Chapter 5: Financial Statements

Chapter 6: Internal Control and Cash

Chapter 7: Long-term Assets

Chapter 8: Liabilities

Chapter 9: Other business entities: Partnerships and Corporations

Chapter 10: The Role of Accounting in the Basic Management Process

Chapter 11: Job Order Costing

Chapter 12: Cost Behavior and CVP Analysis

Chapter 13: Budgeting

Chapter 14: Differential Analysis: Relevant Costs

Chapter 1 Learning Objectives

By the end of this lesson, you will be able to:

- LO1: Define the purpose of accounting

- LO2: Describe the accounting process.

- LO3: Describe the forms of businesses.

- LO4: Define the different types of business entities.

- LO5: Classify the different types of business activities.

- LO6: Identify the four basic financial statements and their purposes

- LO7: Define assets, liabilities, and Owner’s equity.

What Is the Purpose of Accounting?

The Purpose of Accounting

The purpose of accounting is to provide financial information to users in order for those users to make decisions. Accounting is often called the “language of business.” Accounting is the means by which financial information is communicated to users. The focus of this text is on the role of accounting in business.

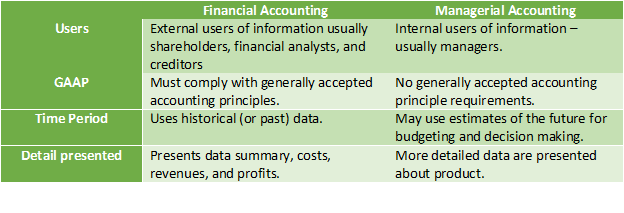

Financial Accounting deals with preparing financial information for external users. Managerial accounting deals with preparing financial information for external users.

Users

Users of accounting information are separated into two groups, internal and external. Internal users are the people within a business organization who use accounting information. External users are people outside the business entity that use accounting information. Accounting information is valuable because decision makers, internal and external, can use it to evaluate the financial decisions of various alternatives. Accountants reduce uncertainty by using professional judgment to quantify the future financial impact of taking action or delaying action. Accounting information plays a significant role in reducing uncertainty within an organization.

Nature and Objective of Business and Accounting

A business is an organization that provides goods or services to customers. The objective of most business is to earn a profit. Profit is the difference between the amount received for selling your goods and services and the cost of providing those goods and services.

Types of Businesses

Three types of businesses operated for profit include service, merchandising (retailers), and manufacturing businesses. Examples of each type of business are below:

Service businesses:

- Federal Express (Delivery services)

- American Airlines (Transportation services)

- Marriott Hotels (Hotel services)

- Universal Studios (Entertainment services)

Merchandising businesses (Retailers):

- Target (general merchandise)

- Amazon (books)

- Walmart (general merchandise)

- Safeway Stores (groceries)

Manufacturing businesses:

- Ford Motor Company (vehicles)

- Dell Inc. (Computers)

Forms of Businesses

A business is normally organized in one of the following four forms:

- proprietorship

- partnership

- limit liability company

- corporation

A proprietorship is an unincorporated business owned and run by one individual with no distinction between the business and the owner. The owner is entitled to all profits and are responsible for ALL business's debts, losses, and liabilities. The primary disadvantage of proprietorships is that the owner has unlimited liability to creditors for the debts of the company. In the United States, more than 70% of all businesses are proprietorships.

A partnership is a legal form of business operation between two or more individuals who share management and profits. The In the United States, about 10% of all business are partnerships. The partners of a partnership also have unlimited liability to creditors for the debts of the company.

A corporation is a legal entity that is separate and distinct from its owners. Corporations enjoy most of the rights and responsibilities that an individual possesses; that is, a corporation has the right to enter into contracts, loan and borrow money, sue and be sued, hire employees, own assets and pay taxes. The ownership of a corporation is represented by shares of stock. A corporation issues the stock to individuals or other entities, who then become owners or stockholders of the corporation. A major advantage of a corporation is that stockholders' have limited liability to creditors for the debts of the company. It is limited to their investment.

A limited liability company (LLC) combines attributes of a partnership and a corporation. The primary advantage of the limited liability company form is that it operates similar to a partnership, but its owners' (or members') liability for the debts of the company is limited to their investment. Many professional practices such as, lawyers, doctors, and accountants are organized as limited liability companies. A Limited Liability company is governed by the State you register the company; this means, it can still function like any of the other businesses entities.

Use the attached resource to see what business structure will best suit your business.

Business Activities

All companies are engaged in the following three business activities:

Operating activities involve the current assets, current liabilities, revenues, and expenses. Revenues are the assets received from selling the company’s goods or services. Revenues are normally identified according to their source.

Investing activities involve buying and selling of company noncurrent assets to start and operate a business. These assets would include land, buildings, computers, office and store machines, office furnishings, trucks, and automobiles.

Financing activities involve obtaining funds to begin and operate a business. Companies obtain funds by:

- issuing shares of stock (Ownership in the business)

- borrowing from the bank

- Issuing bonds (borrowing from the public)

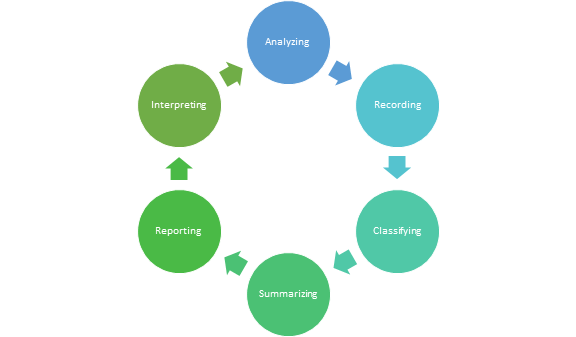

Accounting Process

Accounting is the systemic gathering of financial information about a business and reporting this information to users. The report can be in the form of financial statements, such as the Profit and Loss (Income Statement), or the Balance Sheet. Also, if the company is publicly traded, they must submit an annual report on the financial state of the company.

There are six major steps in this process:

- Recording: entering financial information about economic events into the accounting system. This system can be a program, such as QuickBooks, that can either be cloud based or downloaded to your desktop.

- Classifying: we must ask ourselves what type of information is this? Is this an invoice or a bill? This will help to sort the financial information.

- Summarizing: providing the information in an easy to understand method.

- Reporting: this would be in the form of the financial statements.

- Interpreting: users will use this information to make decisions.

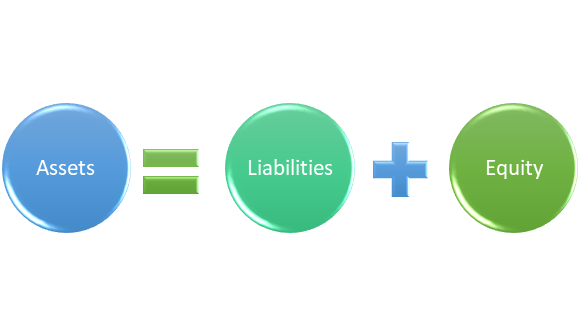

The Accounting Equation

There is a delicate balancing of the financial information; we will use the Accounting Equation to stay in balance. The Accounting Equation is:

The left side shows the assets or economic resour

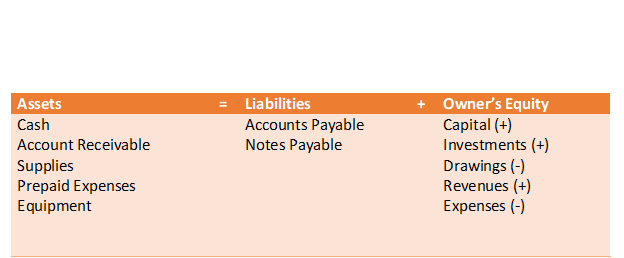

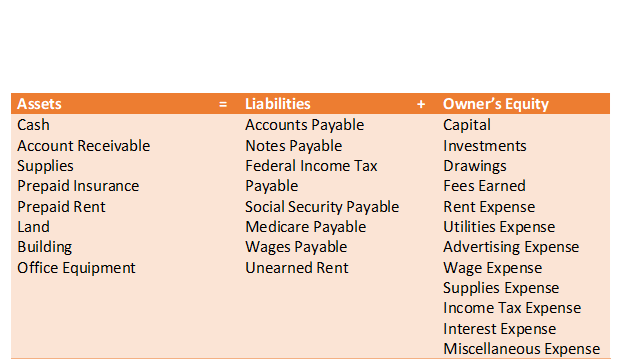

Classifying Accounts Examples

The table shown below lists some of the main account names we will use. As we move forward, the list of accounts will increase.

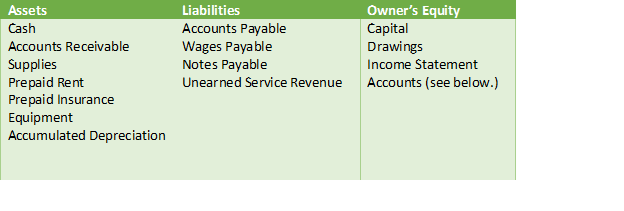

Assets:

- Current assets are cash and other assets that are expected to be converted to cash or sold or used up within one accounting period which is normally one year or less. This would normally include cash, accounts receivable, notes receivable, supplies, and prepaid expenses.

- Long-term assets: Property, Plant, and Equipment are physical assets of a long-term nature. The fixed assets may also be reported on the balance sheet as property, plant, and equipment or plant assets. Fixed assets include equipment, machinery, buildings, and land. Except for land, these assets depreciate over a period of time. The cost less accumulated depreciation is called the book value and is normally reported on the classified balance sheet.

- Intangible assets represent rights of a long-term nature, such as patent rights, copyrights, and goodwill. This will be discussed in different chapter.

Liabilities:

- Current liabilities are liabilities that are due within one accounting period, which is normally one year or less, and are to be paid out of current assets. Normally current liabilities include accounts payable, notes payable, wages payable, interest payable, taxes payable, and unearned revenue.

- Long-term Liabilities are liabilities that are due after the first accounting period.

Owner's Equity:

Owner's equity will be the difference between your assets minus your liabilities (debt) that the owner of the business can claim. This can be derived from the investments, net income less the dividends, that is retained in the business. The owner can decide to withdraw some of the equity in the company.

Taking It Further with Technology

We have learned the basics of Accounting using the pen to paper method but, we know technology affects every aspect of your life. Even in the world of business, we have different devices or programs that help us to run our business. Let's explore them.

Social Media

Social media is a way for a business owner to connect with customers and find new customers. The benefits of using social media can save a company advertising cost by creating their own media. One of the other benefits of social media is you can gain loyal customers; all of the these options are advatanges to social media. One of the disadvantages is the time it takes to learn all the different platforms. Thankfully, there are tech companies that you can purchase already created content and post it own your social media page.

Customer Relationship Management

CRM's will help a company to streamline communication with customers as well as staff. These programs help to orgainize and automate your customer interactions. The scale of the program you select can depend on cost and needs of the company.

Collecting Payments

Paying for services or purchases has become easier with the use of these payment apps. As a customer, you can send money or pay for services from a business. As a business owner, you can use these apps to collect fees and increase your sales because you take different forms of payment.

Virtual Office Assistants and Virtual Offices

When the Pandemic hit, every company had to find a way for work to continue; those that could, started to work remote. This caused companies to address what "working from home" means and how to sufficiently get the work done; companies scrammbled to get equipment and laptops to employees. Businesses saw a huge benefit for some employees to work from home because employees were more productive and it was saving some operational costs. Some companies laid off employees.

Even now that some employees are back at the physical office, this created a new administrative position called a Virtual Assistants; the employee can work from home, using their own equipment, and work for more than just one company at any location. This also caused a huge wave with virtual offices; now, you can complete work from a remote location, using technology to keep appointments and conduct virtual meetings. Keeping information in one place is easy with cloud storage.

There are so many apps or programs you can use to run your business efficiently, it just takes some research to see what apps or programs works best for your business.

Comprehensive Problem

This Comprehensive Problem will span the entire textbook starting as a service company, then, a merchandising company, and lastly, a manufacturing company. This will also serve an an example of the graded comprehensive problem you will compelete as an exam grade.

Foundation

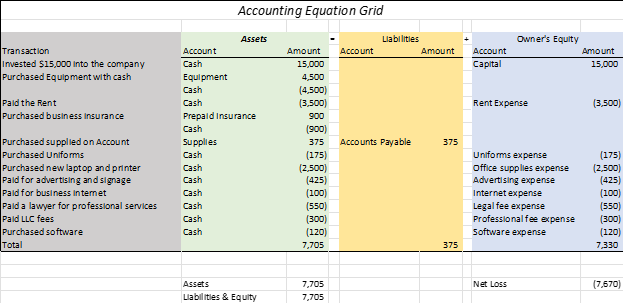

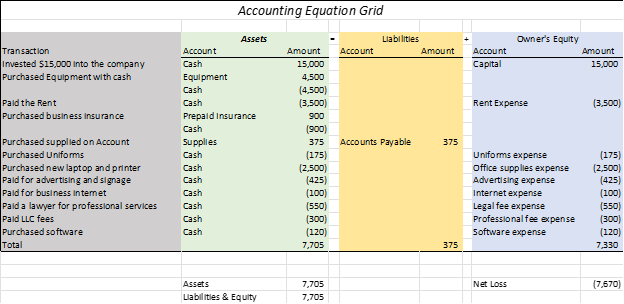

Theia Ellis worked in the field as a Physical Therapist until the Pandemic; she found herself out of a job, even though she loved her patients and her work. Her patients loved her as well, stating they would follow her to another facility. After going on serveral job interviews, she decided to open her own business. With the money from her servant's package and her savings, she invested $15,000, acquired some used equipment from Facebook Marketplace for $4,500, and went in search of an office location. She wanted some place her clients would feel safe and private to conduct sessions. She found a place with private suites and an open space for sessions; the rent and utilities would be $3,500 a month. The other monthly expenses were:

- Business insurance $900 a year

- Supplies - $375

- Uniforms - $175

- New laptop and printer - $2,500

- Advertising and signage - $425

- Internet - $100/month

- A lawyer to complete the formation papers for the LLC - $550

- LLC fee - $300

- EMR system - $120/month

After consulting with a lawyer, Proficient Therapy LLC was formed; the doors will open on Jan. 1. Theia signed the lease for the unit, paying the first month's rent and purchased all the necessary items for the business to start. Using the Accounting equation, it will look like this:

As you can see, Theia has a starting net loss because no revenue has been earned. We will use this information when we check back in with Proficient Therapy.

Chapter 1 Summary

We have discused the basic foundation of Accounting using the Accounting Equation, Assets = Liabilities + Owner's Equity. We will start off by viewing the information from a the sole proprietorship's perspective. We will slowly add new concepts and materials each week. After each chapter, please return to Blackboard to complete your chapter assignments in OHM.

Chapter 2: Analyzing Transactions using the Accounting Equation

LO1: Describe the chart of accounts.

LO2: Describe and illistrate the journalizing transactions using the expanded equation grid.

LO3: Describe and illistrate the journalizing transactions using T accounts.

LO4: Prepare an Unadjusted Trial Balance.

The Chart of Accounts

As we seen in chapter 1, the Chart of Accounts can be extensive depending on the industry or the company. Even so, the Chart of Accounts will have a basic format that most companies will use.

A group of accounts for a business entity is called a ledger; the list of accounts in the ledger is called a Chart of Accounts. The accounts are listed in the order they appear in the Balance Sheet.

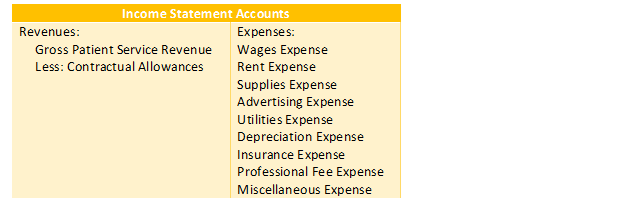

Income Statement:

Revenues. Some may ask, what does revenue mean? This means the way the business makes money. For example, if you sell product, you would have a Sales account in your chart of accounts or you can also have an inventory account because you purchase product.

Expenses. You will use, consume, or expire the prepaid assets of the company to generate revenue, such as, Prepaid Rent or Prepaid Insurance. This means you have paid for this upfront and will use, consume, or expire a flat amount each month and it will be listed on your Income Statement in the "Expenses" area. Also, to generate revenue, you will use expenses; for example, you paid for some advertising to generate customers; this will be classified as Advertising expense. The expenses are listed in order from greatest to least and Miscellaneous Expense will always be last.

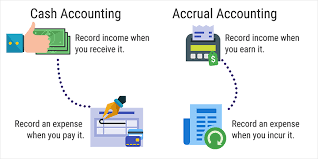

Accrual Accounting and Cash Basis Accounting

What Is Accrual Accounting?

Accrual accounting is an accounting method that records revenue when earned and records expenses when incurred regardless of when cash is received or paid to the Income Statement. Companies often earn revenue before or after cash is received and incur expenses before or after cash is paid. Accrual basis accounting is designed to avoid misleading information arising from the timing of cash receipts and payments.

What is Cash Accounting?

Cash accounting is an accounting method that reports revenue when it is received and when expenses are paid to the Income Statement; this may not happen in the same period the services or expenses were made.

Quickbooks offers a detailed breakdown of Accrual Basis Vs. Cash Basis.

For this class, we will focus on Accrual Accounting.

GAAP

The four corporate financial statements described and illustrated in chapter 1 were prepared using accounting “rules,” called generally accepted accounting principles (GAAP). Generally accepted accounting principles (GAAP) are necessary so that stakeholders can compare companies across time. If the management of a company could prepare financial statements as they saw fit, the comparability between companies and across time would be impossible.

Accounting principles and concepts develop from research, accepted accounting practices, and pronouncements of regulators. Within the United States, the Financial Accounting Standards Board (FASB) has the primary responsibility for developing accounting principles. The FASB publishes Statements of Financial Accounting Standards as well as interpretations of these Standards.

The Securities and Exchange Commission (SEC), an agency of the U.S. government, also has authority over the accounting and financial disclosures for corporations whose stock is traded and sold to the public. The SEC normally accepts the accounting principles set forth by the FASB. However, the SEC may issue Staff Accounting Bulletins on accounting matters that may not have been addressed by the FASB.

Many countries outside the United States use generally accepted accounting principles adopted by the International Accounting Standards Board (IASB).

Accounting Principles and Concepts

Business Entity Concept: The business entity concept limits the economic data recorded in an accounting system to data related to the activities of that company. In other words, the company is viewed as an entity separate from its owners, creditors, or other companies. For example, a company with one owner records the activities of only that company and does not record the personal activities, property, or debts of the owner. A business entity may take the form of a proprietorship, partnership, corporation, or limited liability company (LLC).

Cost Concept: The cost concept initially records assets in the accounting records at their cost or purchase price.

Going Concern Concept: The going concern concept assumes that a company will continue in business indefinitely. This assumption is made because the amount of time that a company will continue in business is not known.

Matching Concept: The matching concept reports the revenues earned by a company for a period with the expenses incurred in generating the revenues. That is, expenses are matched against the revenues they generated.

Revenue Recognition Principle: Revenues are normally recorded at the time a product is sold or a service is rendered, which is referred to as the revenue recognition principle. At the point of sale, the sale price has been agreed upon, the buyer acquires ownership of the product or acquires the service, and the seller has a legal claim against the buyer for payment.

Unit of Measure Concept: In the United States, the unit of measure concept requires that all economic data be recorded in dollars. Other relevant, non-financial information may also be recorded, such as terms of contracts. However, it is only through using dollar amounts that the various transactions and activities of a business can be measured, summarized, reported, and compared. Money is common to all business transactions and thus is the unit of measurement for financial reporting.

Adequate Disclosure Concept: The adequate disclosure concept requires that the financial statements, including related notes, contain all relevant data a stakeholder needs to understand the financial condition and performance of the company. Nonessential data are excluded to avoid clutter.

Accounting Period Concept: The accounting period concept requires that accounting data be recorded and summarized in financial statements for periods of time. For example, transactions are recorded for a period of time such as a month or a year.

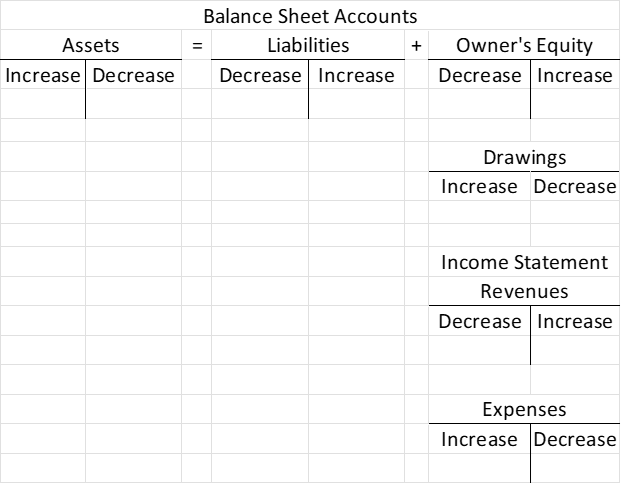

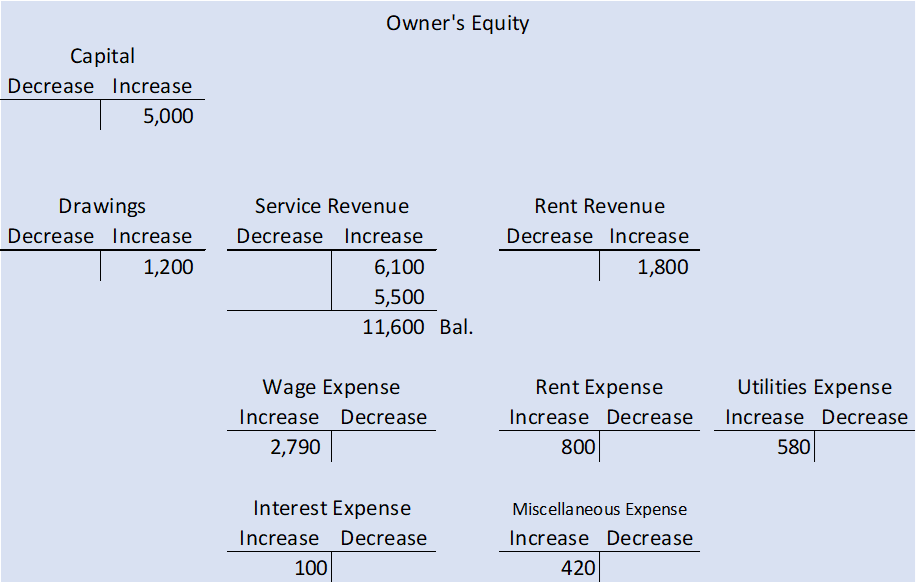

Transaction Analysis

We will use the extended version of the Accounting Equation to evaluate transactions using T accounts. As you can see, we implemented the Equation with an "Increase" or "Decrease"; once you go to the other side of the equal, the "Increase" and Decrease flip.

Examples of Transactions

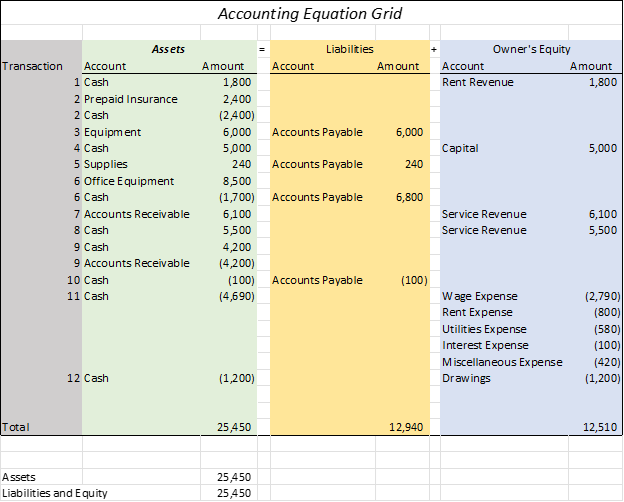

To illustrate accrual accounting, the following transactions are used for Landry Medical Group:

- Received $1,800 from ILS Company as rent for the parking lot.

- Paid a premium of $2,400 for a two-year general business insurance policy that covers risks from fire and theft.

- Purchased a new piece of equipment for $6,000 on account.

- Dr. Landry invested an additional $5,000 in the business.

- Purchased supplies for $240 on account.

- Purchased $8,500 of office equipment. Paid $1,700 cash as a down payment, with the remaining $6,800 ($8,500 − $1,700) due in five monthly installments of $1,360 ($6,800 ÷ 5).

- Provided services of $6,100 to patients on account.

- Received $5,500 for services provided to patients who paid cash.

- Received $4,200 from insurance companies on patients' accounts for services that were provided in transaction 7.

- Paid $100 on account for supplies that were purchased in transaction 5.

- Expenses paid during November were as follows: wages, $2,790; rent, $800; utilities, $580; interest, $100; and miscellaneous, $420.

- Personally withdrew $1,200.

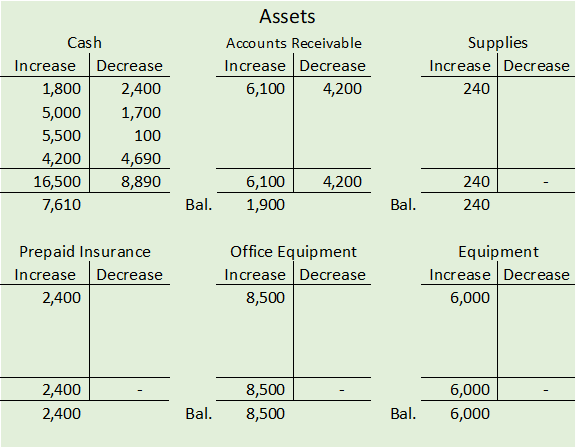

Breaking It Down - Assets

Here's the Assets listed in the T accounts:

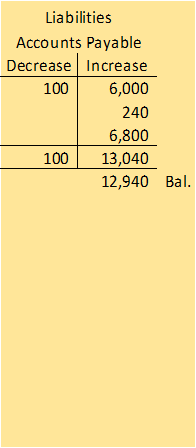

Breaking It Down - Liabilities and Equity

Adjustments

The Adjustment Process

Accrual accounting requires the updating of the accounting records prior to preparing financial statements. This updating is called the adjustments. Adjustments are necessary because, at any point in time, some accounts of the accounting equation are not up to date. The income statement of a business reports all revenues earned and all expenses incurred to generate those revenues during a given period. An income statement that does not report all revenues and expenses is incomplete, inaccurate, and possibly misleading. Similarly, a balance sheet that does not report all of an entity’s assets, liabilities, and stockholders’ equity at a specific time may be misleading. Each adjustment has a dual purpose: (1) to make the income statement report the proper revenue or expense and (2) to make the balance sheet report the proper asset or liability. Thus, every adjustment affects at least one income statement account and one balance sheet account.

The accounts that need adjusting are:

- Deferrals are the result of cash being received or paid before the revenue is earned or the expense is incurred.

- Accruals are normally the result of cash being received or paid after revenue has been earned or an expense has been incurred.

- Prepaid or deferred expenses: Initially recorded assets but become expenses over time or through normal operations of business. Examples include prepaid insurance and prepaid advertising.

- Unearned or deferred revenues: Initially recorded as liabilities but become revenues over time or through normal operations of the business. Examples include unearned rent and insurance premiums received in advance.

- Accrued expenses or liabilities: Expenses that have been incurred but are not recorded in the accounts. Examples include unpaid wages and utility expenses.

- Accrued revenues or assets: Revenues that have been earned but are not recorded in the accounts. Examples include revenue for patient services that have been earned but are not recorded in the accounts and accrued interest on notes receivable.

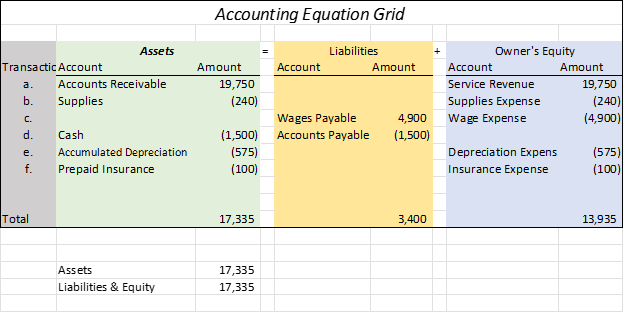

Adjustment Example

Let's make the end of the period adjustments for Landry Medical Group.

- Service revenue accrued but unbilled - $19,750.

- Used up all the supplies in the Supplies account.

- Wages accrued but not paid - $4,900

- Paid $1,500 to creditors; this will pay the remaining balance in supplies and make the first installment payment.

- Depreciation of equipment - $575

- Insurance expired - $100

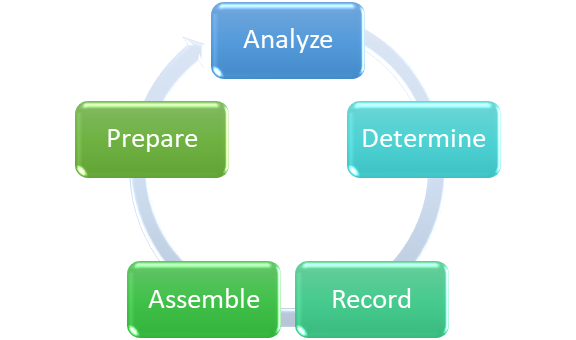

Accounting Cycle

The accounting cycle is the process that goes through the following steps:

- Analyze the source documents (checks, contracts, invoices, etc.)

- Determine what accounts are affected (Assets, Liabilities, and Owner’s Equity).

- Determine if the accounts are increasing or decreasing and how each transaction affects the financial statements (Income Statement, Statement of Owner's Equity, Balance Sheet, and Statement of Cash Flows). Record the economic transactions.

- Assemble adjustment data and record those adjustment to the accounts.

- Prepare the financial statements.

Comprehensive Problem

Let's check in with Theia Ellis, owner of Proficient Therapy LLC.

Here is the information for Proficient Therapy LLC:

Here are the transactions for the Month of January:

Jan.

4. Provided services for clients on account, $9,400; we will use Gross Patient Service Revenue.

5. Purchased additional equipment for $7,000, paying a down payment of $1,000 and making monthly installments of $500 for one year.

7. Received $ 3,760 from the insurance companies for Jan. 4.

10. Created a Groupon advertisement giving patients 20% off services; this will be cash paying clients.

14. Paid wages to part-time workers, $ 1,825.

15. The Groupon was a success! Received $11,700 in advance payment for services; we will record this as unearned revenue.

16. Paid $375 to the Office Depot credit card.

18. Recorded services provided to clients on account, $ 3,625.

20. Purchases more supplies on account from Office Depot, $1,265.

24. Met with the manager of a nursing home to come by twice a week to provide services to the patients. The contract was for a flat rate of $2,000 per month for 3 months; received $6,000.

26. Paid for my professional membership dues of $380.

27. Paid wages to part-time workers, $1,825.

29. Paid utilities of $760.

30. Withdrew $1,750 for personal use.

Using the information, enter the economic transactions into GNU cash program. Use the Accounts below:

Adjusting entries for the month of January:

- Insurance expired during January is $75.

- Supplies on hand on January 31 are $759.

- Made the first installment payment of $500.

- Depreciation of equipment is $ 250.

- Some Groupon clients came in for services, $3,510.

- Groupon collected their fee from adjustment (e): $1,755

- Accrued wages of $1,095.

- Earned $1,000 from transaction 24.

Chapter 3: Receivables

In this lesson you will be able to account for receivables and short term investments and you will be able to:

- Distinguish between the direct write off and allowance methods.

- Determine the financial statement effects accounting for uncollectible accounts using the direct write off and allowance methods.

- Analyze the notes receivable transactions and effects on the financial statements

Accounts Receivable

Accounts Receivable

All receivables expected to be realized in cash within a year are presented in the Current Assets section of the balance sheet. These assets are normally listed in the order of their liquidity, that is, the order in which they are expected to be converted to cash during normal operations.

The usual transaction creating a receivable is selling merchandise or services on account (on credit). This is recorded as an increase to Accounts Receivable. These accounts are normally collected within 30 or 60 days. They are classified on the balance sheet as a current asset.

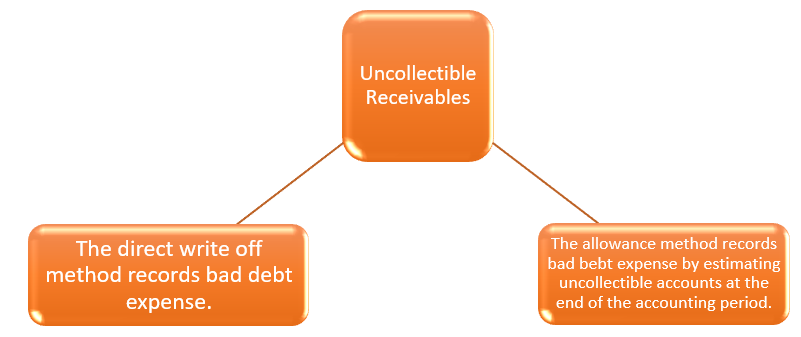

Uncollectible Receivables

Uncollectible Receivables

A major concern about accounts receivable is that some customers will not pay their accounts and may become uncollectible.

- Companies may shift the risk of uncollectible receivables to by accepting major credit cards like American Express, Discover, MasterCard or VISA. This shifts the risk to the credit card companies.

- Companies may also sell their receivables to a buyer of receivables called a factor. The risk may shift to the factor.

Many companies will grant credit to their customers. Regardless how well you check for customers, some credit sales will be uncollectible. When an account is uncollectible it is recorded as a bad debt expense.

There are two methods of accounting for uncollectible receivables are as follows:

Direct Write-off Method:

General accepted accounting principles (GAAP) do not recognized the direct write-off method. Under the direct write-off method, bad debt expense is recorded when the customer's account is determine to be uncollectible. At that time, the customer's account receivable is written off.

Uncollectible Receivables: the Allowance Method

The two allowance methods used to estimate uncollectible accounts are as follow:

Percentage of the Accounts Receivable Method

The allowance method estimates the uncollectible accounts receivable at the end of the accounting period. Based on this estimate, Bad Debt Expense is recorded by an adjustment.

Percentage of the Sales Method

The percent of sales method assume that a percent of the credit sales is uncollectible. This percent can come from industry standards or historical trends from the company.

The Importance

The importance of keeping up with how much Accounts receivable is uncollected because there is cash on the line. The longer you wait to collect payment, the more you lose to collect. Please read the following article on Aging of Receivables.

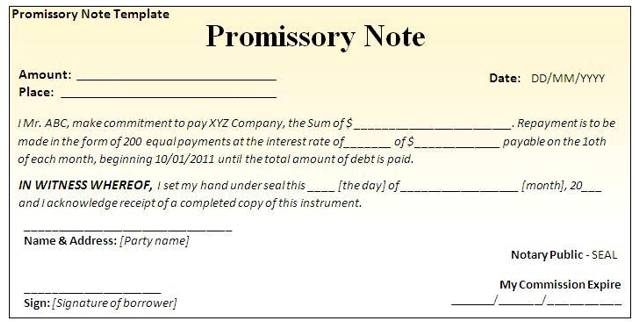

Notes Recievable

Notes receivable are amounts that customers owe for which a legal, written document is issued. If notes receivable are expected to be collected within a year, they are classified on the balance sheet as a current asset.

Parts of a promissory note are as follows:

- The maker is the party making the promise to pay.

- The payee is the party to whom the note is payable.

- The face amount is the amount the note is written for on its face.

- The issuance date is the date a note is issued.

- The due date or maturity date is the date the note is to be paid.

- The term of a note is the amount of time between the issuance and due dates.

- The interest rate is that rate of interest that must be paid on the face amount for the term of the note.

The interest rate is stated on an annual (yearly) basis, while the term is expressed in days. Thus, the interest and maturity value on the note in computed as follows: Principle X Rate X Time.

To simplify, 360 days per year are used in this chapter. In practice, companies such as banks and mortgage lenders use the exact number of days in a year, 365.

The maturity value is the amount that must be paid at the due date of the note, which is the sum of the face amount and the interest. You will hear the word for face to also mean principle.

The maturity date will be counting the days left in the month it is issued and counting the days for each month until you have accumulated the total days.

| January- 31 | July - 31 |

| Feb- 28 | August - 31 |

| March - 31 | September - 30 |

| April - 30 | October - 31 |

| May - 31 | November - 30 |

| June - 30 | December - 31 |

For example, Roberts Company issued a $40,000, 6%, 45 day note on Feb.1 to Peoples Inc.

We will use the formula Principle X Rate X Time to calculate the amount of interest: $40,000 X 0.06 X (45/360) = 300

Now, to calculate the due date we will look at the table to count the 45 days; let's determin the due date of the note:

| Number of days in the Note | 45 |

| Days remaining in February | 28 |

| Days remaining in March | 17 |

| Due date of the Note | March 17th |

Therefore, on March 17, Peoples Inc will pay the maturity value, face + interest, to Roberts Company.

Notes may be used to settle a customer's account receivable. Notes and accounts receivable that result from sales transactions are sometimes called trade receivables. All notes and accounts receivable in this chapter are assumed to be from sales transactions.

Chapter 4: Merchandise Inventory

You will be able to describe the basis for inventory valuation and you will be able to:

- Define merchandise inventory.

- Calculate ending inventory and cost of goods sold under the periodic inventory system using FIFO, LIFO, Weighted Average methods.

- Describe factors considered when selecting and inventory method and the effects of such a selection on the financial statements.

Merchandising Business

The revenue activities of a merchandising business involve the buying and selling of inventory (merchandise for resale). When the merchandise is purchased, it is shown on the balance sheet as a current asset. A retail business first purchases merchandise to sell to its customers. When this inventory is sold, the revenue is reported as sales revenue. The cost of the inventory sold is reported as cost of goods sold. The cost of goods sold is subtracted from sales revenue to arrive at gross profit. The operating expenses are subtracted from gross profit to arrive at operating income.

Sales Transactions

Cash Sales Transactions: Sales transactions may be a cash sale or credit sale. Cash sales are recorded in the accounts by increasing cash and sales. Under the perpetual inventory system, Cost of goods sold should be increased and merchandise inventory should be decrease in the same transaction. Credit card sales using VISA, MasterCard, or American Express are recorded as cash sales with a reduction of the credit card fees.

Credit Sales: Credit sales are recorded in the accounts by increasing accounts receivable and sales. Increasing the cost of goods sold and decreasing inventory should also be made in the same transaction.

Sales Discounts: A merchandiser may grant customers sales discounts as incentives to encourage them to pay their bills early. For example, a seller may offer credit terms of 2/10, n/30, which provides a 2% sales discount if the invoice is paid within 10 days. If not paid within 10 days, the total invoice amount is due within 30 days. A buyer refers to a sales discount as a purchases discount.

The revenue recognition principle requires that revenue be recorded in the amount expected to be received from the sale. Therefore, sales revenue should be recorded net of the sales discount.

Sales Returns and Allowances: Merchandising companies usually allow customers to return goods that are defective or unsatisfactory for a variety of reasons, such as wrong color, wrong size, wrong style, wrong amounts, or inferior quality. In fact, when their policy is satisfaction guaranteed, some companies allow customers to return goods simply because they do not like the merchandise. A sales return is merchandise returned by a buyer. Sellers and buyers regard a sales return as a cancellation of a sale. Alternatively, some customers keep unsatisfactory goods, and the seller gives them an allowance off the original price. A sales allowance is a deduction from the original invoiced sales price granted when the customer keeps the merchandise but is dissatisfied for any of a number of reasons, including inferior quality, damage, or deterioration in transit. When a seller agrees to the sales return or sales allowance, the seller sends the buyer a credit memorandum indicating a reduction (crediting) of the buyer's account receivable.

Sales Tax

Sales Taxes Almost all states levy a sales tax on sales of merchandise inventory. A sales tax is levied on the final user of a product. Buyers who purchase product to resale do not have to pay a sales tax. That is referred to as buying it wholesale. When a sale is made on account or for cash, the seller charges the buyer by increasing Accounts Receivable or cash to the total sales plus sales tax, increasing the sales revenue for the amount of the sales, and increasing sales tax payable for the sales taxes.

Purchasing Inventory

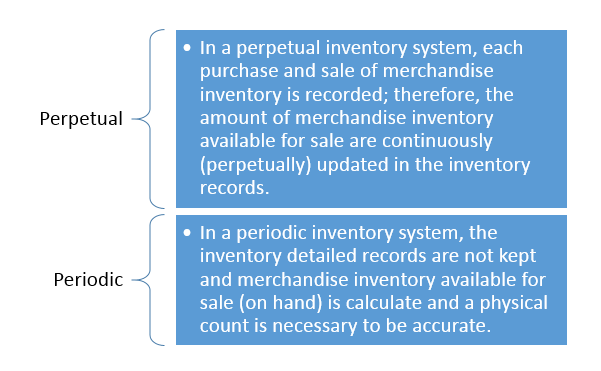

There are two systems for recording and accounting for merchandise inventory: perpetual and periodic.

In either case, perpetual or period, an inventory physical count must be taken and compared to the records. This physical inventory is used to determine the cost of inventory on hand at the end of the period, which is the amount reported as Inventory on the balance sheet.

Purchase Discounts

Purchases Discounts: Normally, the purchaser of inventory will take the discounts taken with the discount period. Purchases discounts are given for early payment of a purchase invoice. The credit terms 2/10, n30 mean that the buyer is entitled to a 2% discount if paid within 10 days (2/10) from the invoice date. If the discount period is missed, the buyer must pay the full invoice within 30 days (n30). In a perpetual inventory system, the merchandise inventory is reduced for the purchase discount.

Purchase Returns and Allowances: Purchases returns and allowances result when merchandise inventory received by a buyer is defective, damaged, or not what was ordered. In these cases, the buyer may return the merchandise for full credit or request a price adjustment (allowance). In a perpetual inventory system, the inventory is reduced for the return or allowance.

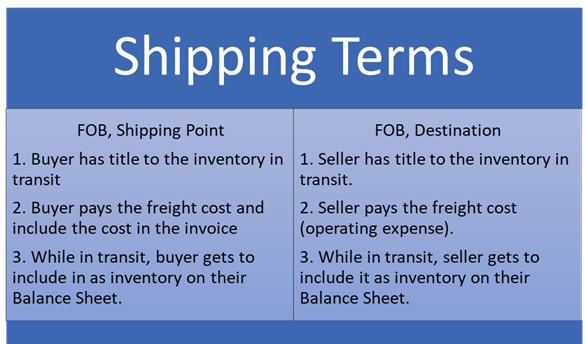

Shipping Terms

Freight Cost: Freight cost (shipping cost) must be paid by either the buyer or the seller. Who pays the freight cost is determined when title (ownership) of merchandise inventory passes. Title may pass to the buyer the seller either delivers to the inventory to the freight carrier or when the buyer received the inventory.

Shipping Terms

We have all purchased goods online, as a consumer, when the rights to the goods can happen in two ways:

- The term FOB (free on board) shipping point means that the title for the goods pass to the buyer when the seller delivers the merchandise inventory to the transportation company. Such costs are part of the buyer's total cost of purchasing inventory and should be added to the cost of the inventory.

- The term FOB destination means that the seller pays the freight costs from the shipping point (seller’s dock) to the final destination. Such cost would be included in the operating expenses as a shipping expense or freight out expense.

Here's an example of how to calculate the different shipping terms.

Below are two invoices received by Theia Ellis; she purchsed some merchandise for her company:

The terms are expressed in 1/10, n/30; this means they get a 1% discount if they pay in 10 days and pay the remainder in 30 days. The shipping terms gives two benefits, first, to the seller because there will be some form of payment either in 10 days or 30 and second, the buyer gets a discount for paying early.

Now, we will calculate how much Theia will pay each invoice:

Invoice #8905654: $2,678.75 ( 2,500 - 375 - 21.25 + 575)

Invoice #4599125: $4,189.50 ( 4,500 - 225 - 85.50)

Inventory Shrinkage

Inventory Shrinkage: Although under the perpetual inventory system, the inventory account is continually updated for purchase and sales transactions, a physical inventory count is necessary. The difference in the physical count and the records is normally caused by loss of inventory due to shoplifting, employee theft, or errors. Thus, the physical inventory on hand at the end of the accounting period is usually less than the balance of Inventory. This difference is called inventory shrinkage or inventory shortage.

Under the perpetual inventory system, the inventory account is continually updated for purchase and sales transactions. As a result, the balance of the inventory account is the amount of merchandise available for sale at that point in time.

Periodic Inventory Method

As mentioned earlier, most company uses the perpetual inventory system; but, for merchandising companies with enormous variety of inventory and cost of a perpetual system is not cost benefit, they may use a periodic inventory system. In a periodic system, cost of goods sold is calculated as follows:

In order to calculate Cost of merchandise purchase, you must replace the entries to Inventory with four (4) new accounts and they are:

- Purchases

- Purchase returns and allowances

- Purchase Discount

- Freight In

To calculate Cost of merchandise purchased is as follows:

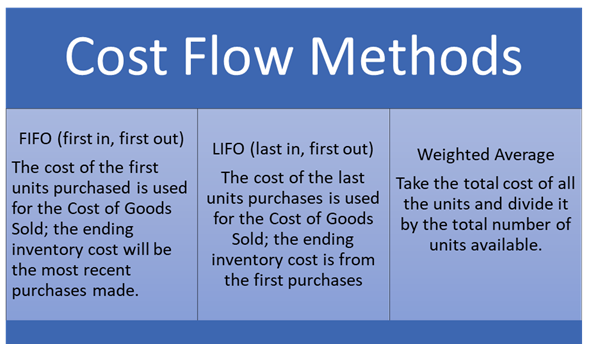

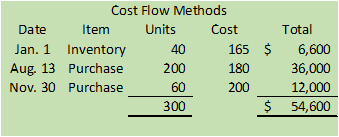

Cost Flow Methods: When identical units of inventory are acquired at various unit costs, it is necessary to determine the cost of the unit sold using various cost flow methods. We will discuss three common cost flow methods using the periodic method in this chapter:

Example

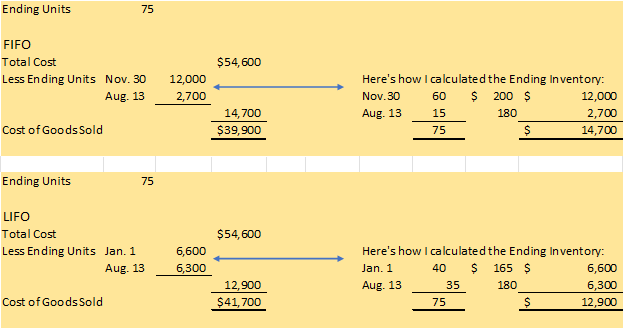

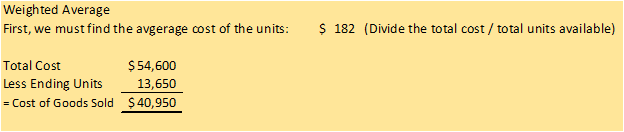

Mama T's Treats purchased some custom mixers to sell online with the company's brand and logo. The information is show below:

After conducting a physical count of the units, only 75 were left; each unit sold for $350.

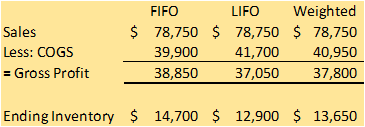

Determine the Cost of Goods Sold, Ending Inventory, and Gross Profit for each of the three methods.

Remember, we're only asking one question, what happened to the inventory? Is it sitting in the warehouse or did we sell it?

Here are the final calculations:

Lower Cost of Market

Generally, companies should use historical cost to value inventories and cost of goods sold. However, “Rule of Conservatism” states the for financial statement purposes, companies should us value inventory items at less than their cost when the market is lower. A decline in the selling price of the goods or their replacement cost may indicate such a loss of utility. This section explains how accountants handle some of these departures from the cost basis of inventory measurement.

The lower-of-cost-or-market (LCM) method is an inventory costing method that values inventory at the lower of its historical cost or its current market (replacement) cost. The term cost refers to historical cost of inventory as determined under the specific identification, FIFO, LIFO, or weighted-average inventory method. Market generally refers to a merchandise item’s replacement cost in the quantity usually purchased. The basic assumption of the LCM method is that if the purchase price of an item has fallen, its selling price also has fallen or will fall. The LCM method has long been accepted in accounting.

Chapter 5: Financial Statements

By the end of this section, you will be able to:

- Prepare a simple: Income Statement, Statement of Retained Earnings, Balance Sheet, and Statement of Cash Flows

- Prepare a Classified Balance Sheet

Delivery of Information

The accounting reports providing this information are called financial statements. The order of the financial statements and the explanation of each statement are listed below:

| Financial Statements | Description | Order of Preparation |

| Income Statement or Profit and Loss | Shows a detail of the revenues and expenses for a specific period of time. | 1 |

| Retained Earnings Statement | Shows a detail of the changes that occurred in the Retained Earnings during a specific period of time. | 2 |

| Balance Sheet | Shows the Accounting Equation ( Assets = Liabilities + Stockholders' Equity) on a specific date in time. | 3 |

| Statement of Cash Flows | Shows the inflows and outflows of the Cash account for a specific period of time. | 4 |

These reports are prepared at the end of an accounting period.

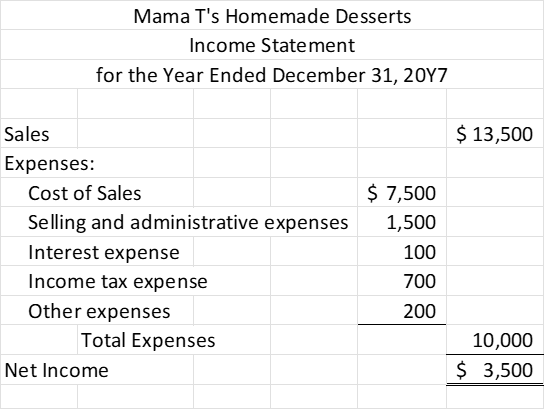

Income Statement

Financial statements present the results of operations and the financial position of the company. Four main statements are commonly prepared by publicly-traded companies and are prepared in the following order:

Income Statement

The income statement reports the results of the operation of the company. The time period covered by the income statement may vary; it can be monthly, quarterly, or yearly. The income statement formula is: revenues minus expenses. Expenses should be listed in the order of the greatest amount first, except for Miscellaneous and Income Tax Expenses should be last.

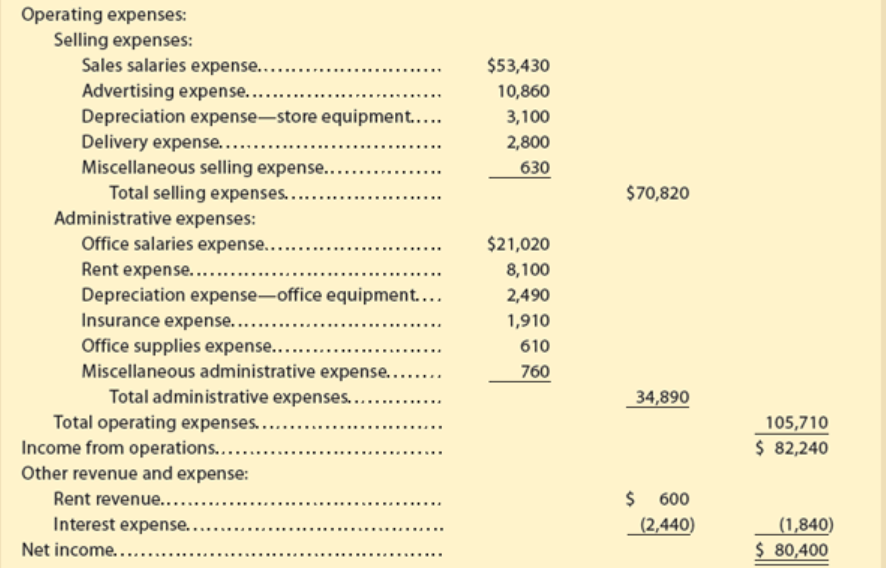

The Multi-step Income

This Income statement will breakdown the expenses to Selling and Administrative; we will use this type of statement to analyze any increases or decreases.

First, we will take Sales and deduct the Sales Discounts and Sales Returns and Allowances to get Net Sales. Next, we deduct the Cost of Goods Sold from it to get the Gross Profit. The Gross Profit represents what we sold the product for minus what we purchased the product for; this will show us the gross amount before we deduct any expenses.

We will break the expenses down as shown in the illistration:

Administrative expenses are general expenses incurred in a normal process of the business such as rent expense, office salaries, depreciation on the office equipment, etc.

Other Revenue and Expenses are items not related to the primary function of the business. For example, If I sold a product but I owned a building and leased out offices, I would put my Rent Revenue in this field.

Retained Earnings (Statement of Owner's Equity)

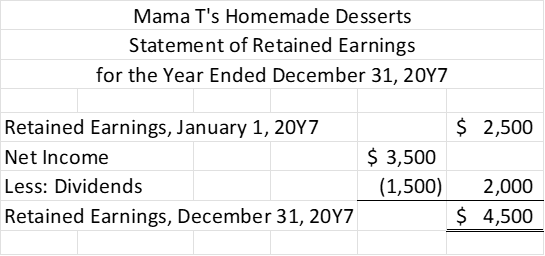

Statement of Retained Earnings

The statement of retained earnings reports the changes in retained earnings. A corporation may retain all of its net income for expanding operations, or it may pay a portion or all of its net income as dividends.

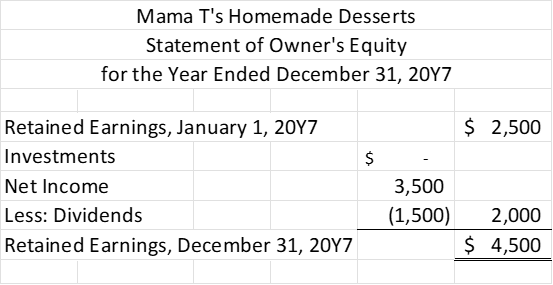

Here's another way to complete the Equity Statement:

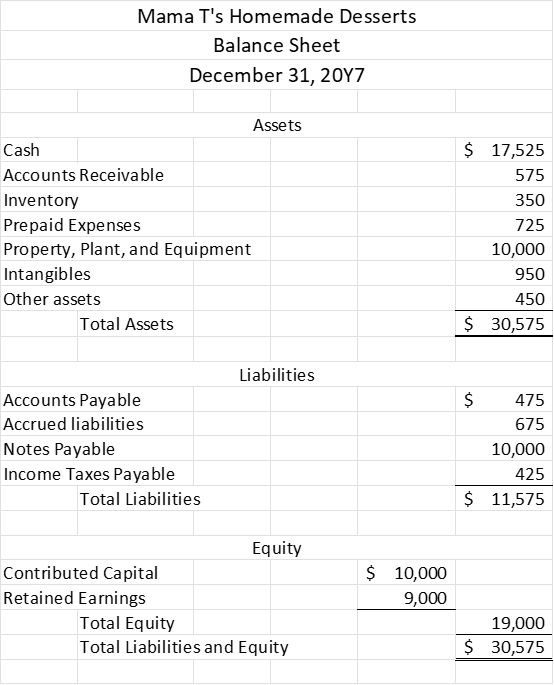

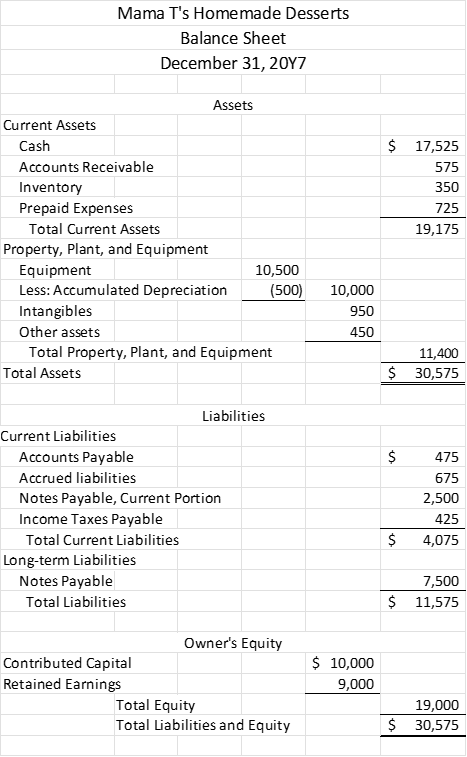

Balance Sheet

Balance Sheet

The balance sheet reports the financial position of the company at a point in time. The financial condition of a business can be expressed as the accounting equation. The balance sheet, sometimes called the statement of financial condition. Assets on the Balance Sheet are listed in the order of liquidity or how quickly consumed.

Classified Balance Sheet

The classified balance sheet is prepared to assist the user in decision making through analysis. Let’s first address the classified balance sheet. The classified balance sheet is prepared with various sections and subsections as follows:

Assets:

- Current assets are cash and other assets that are expected to be converted to cash or sold or used up within one accounting period which is normally one year or less. This would normally include cash, accounts receivable, notes receivable, supplies, and prepaid expenses.

- Long-term assets: Property, Plant, and Equipment are physical assets of a long-term nature. The fixed assets may also be reported on the balance sheet as property, plant, and equipment or plant assets. Fixed assets include equipment, machinery, buildings, and land. Except for land, these assets depreciate over a period of time. The cost less accumulated depreciation is called the book value and is normally reported on the classified balance sheet.

- Intangible assets represent rights of a long-term nature, such as patent rights, copyrights, and goodwill. This will be discussed in chapter 6.

Liabilities:

- Current liabilities are liabilities that are due within one accounting period, which is normally one year or less, and are to be paid out of current assets. Normally current liabilities include accounts payable, notes payable, wages payable, interest payable, taxes payable, and unearned revenue.

- Long-term Liabilities are liabilities that are due after the first accounting period.

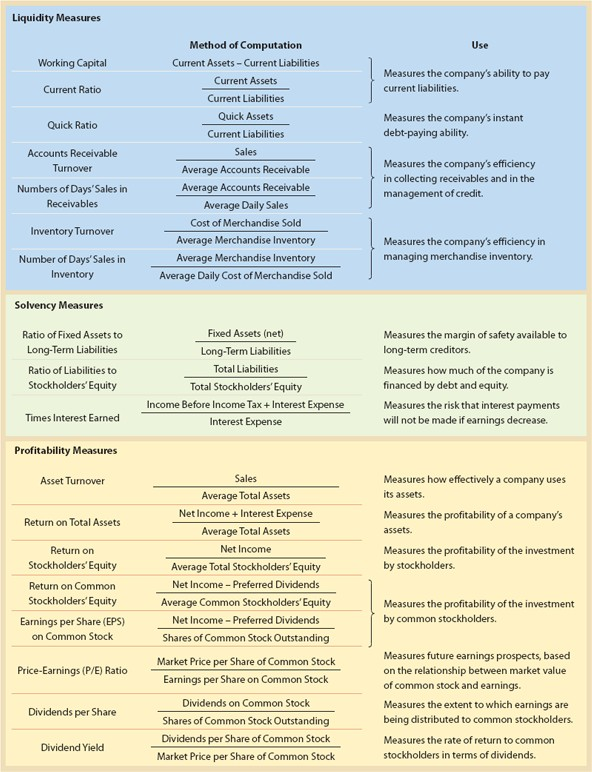

Analysis: At this time we will discuss a few liquidity measures. The ability to pay current debt is important. The Quick Ratio, Current Ratio, and Working Capital calculation let the users know if they have enough current assets to pay current liabilities.

Working Capital

The Working Capital is the excess of the current assets minus the current liabilities; it will show if a company has pay it's current obligations or liabilities. The Working Capital can be express in dollars; the formula to express Working Capital in dollars is: Current Assets - Current Liabilities. To express the Working Capital in a ratio is called Current Ratio; the formula to express Current ratio is: Current Assets/Current Liabilities.

Quick Ratio

The Quick Ratio looks at the "quick" assets, Cash, termorary investments, and receivables, and divide it by current liabilities. This can also be referred to as the acid-test ratio.

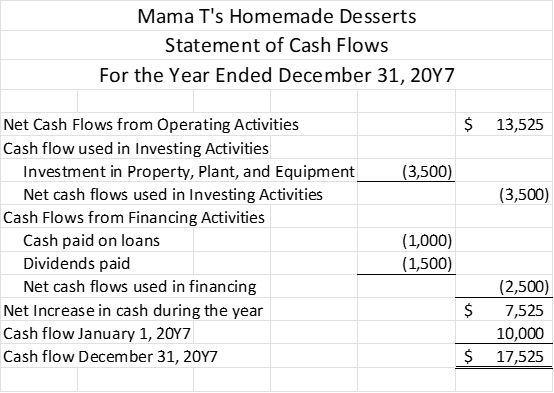

Statement of Cash Flow

Statement of Cash Flows

The statement of cash flows reports the change in the balance sheet due to the changes in cash during a period. The statement of cash flows looks at the three business activities of operating, investing, and financing. Any changes in cash must be related to one or more of these activities.

Operating Activities: The most important cash flow is from the operating activities. The net cash flows from operating activities is reported first. Operating activities are associated with cash flow from the company’s income statement. Bankers and creditors look at the cash flow from operating activities to see if the operating activities are generating enough cash In the short term, creditors use cash flows from operating activities to assess whether the company's operating activities are generating enough cash to repay them. In the long term, a company cannot survive unless it generates positive cash flows from operating activities. Thus, cash flows from operating activities is also a focus of employees, managers, suppliers, customers, and other stakeholders who are interested in the long-term success of the company.

Investing Activities: The net cash flows from investing activities is reported second. This is because investing activities directly impact the operations of the company. Cash receipts from selling property, plant, and equipment are reported in this section. Likewise, any purchases of property, plant, and equipment are reported as cash payments. Companies that are expanding rapidly, such as start-up companies, normally report negative net cash flows from investing activities. In contrast, companies that are downsizing or selling segments of the business may report positive net cash flows from investing activities.

Financing Activities: The net cash flows from financing activities is reported third. Any cash receipts from issuing debt or stock are reported in this section as cash receipts. Likewise, cash payments of debt and dividends are reported in this section.

The statement of cash flows is completed by adding the net cash flows from operating, investing, and financing activities to determine the net increase or decrease in cash for the period. This net increase or decrease in cash is then added to the cash at the beginning of the period to arrive at the cash at the end of the period.

Financial Statement Analysis

Management’s analysis of financial statements primarily relates to parts of the company. Using this approach, management can plan, evaluate, and control operations within the company. Management obtains any information it wants about the company’s operations by requesting special-purpose reports. It uses this information to make difficult decisions, such as which employees to lay off and when to expand operations. Our primary focus in this chapter, however, is not on the special reports accountants prepare for management. Rather, it is on the information needs of persons outside the firm.

Investors, creditors, and regulatory agencies generally focus their analysis of financial statements on the company as a whole. Since they cannot request special-purpose reports, external users must rely on the general-purpose financial statements that companies publish. These statements include a balance sheet, an income statement, a statement of stockholders’ equity, a statement of cash flows, and the explanatory notes that accompany the financial statements.

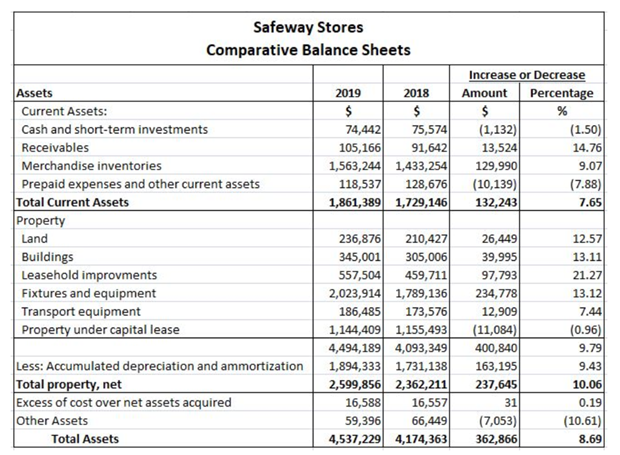

Financial Statement Analysis: Horizontal Analysis

Financial statement analysis consists of applying analytical tools and techniques to financial statements and other relevant data to obtain useful information. This information reveals significant relationships between data and trends in those data that assess the company’s past performance and current financial position. The information shows the results or consequences of prior management decisions. In addition, analysts use the information to make predictions that may have a direct effect on decisions made by users of financial statements.

Comparative financial statements present the same company’s financial statements for one or two successive periods in side-by-side columns. The calculation of dollar changes or percentage changes in the statement items or totals is horizontal analysis. This analysis detects changes in a company’s performance and highlights trends.

The good news is you have already been performing the first part of horizontal analysis without realizing it when you were preparing the statement of cash flows. Horizontal analysis consists of 2 things:

- Dollar amount of change (calculated as Current Year amount – Previous Year amount)

- Percentage of change (calculated as Dollar amount of change / previous year amount)

Horizontal analysis is called horizontal because we look at one account at a time across time. We can perform this type of analysis on the balance sheet or the income statement.

This example from Safeway Stores shows a horizontal analysis balance sheet. Image source: Author

Source: playaccounting.com.

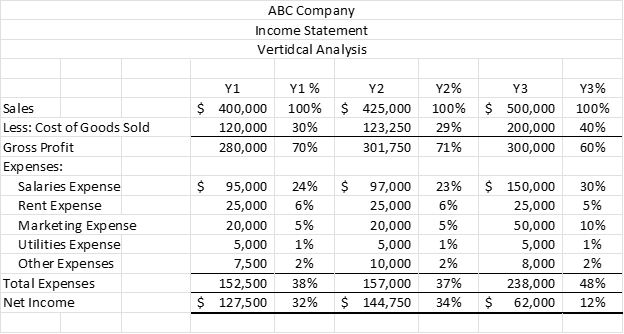

Financial Statement Analysis: Vertical Analysis

Vertical analysis is a method that expresses each item on the financial statements as a percentage of a base. The base on the income statement is sales and the base on the balance sheet is total assets or total liabilities and stockholders’ equity.

Other Financial Analyses

Other analyses of the company's financial condition and performance are normally analyzed and interpreted by focusing upon the following characteristics:

- Liquidity is the ability to convert assets to cash. Short-term creditors such as banks and suppliers focus on a company's liquidity as a means of evaluating the ability of the company to pay short-term debt.

- Solvency is the ability of a company to pay its long-term debts. Investors in bonds and banks, focus on a company's solvency as a means to evaluate the ability of the company to pay both the interest and the principle on long-term debt.

- Profitability is the ability of a company to generate net income.

Chapter 6: Internal Control and Cash

At the end of the chapter, you will be able to:

- Understand Fraud

- Sarbanes-Oxley Act and its impact on controls and financial reporting.

- Internal controls procedures that provide a reasonable assurance that the financial statements can be relied on.

- Bank reconciliation that determines if the general ledger balance for cash is correct.

Fraud

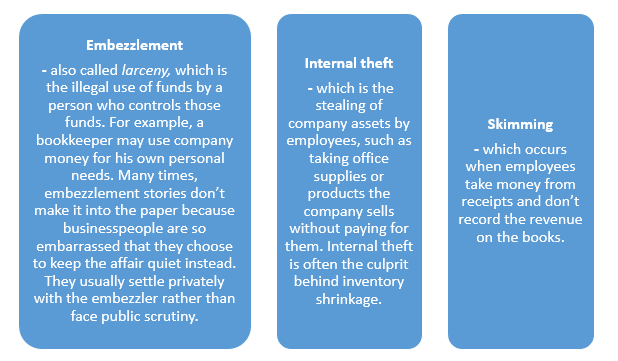

Fraud occurs when an employee gains something of value, usually money or property, at a cost to the employer by knowingly making a misrepresentation of a matter of fact. Fraud commonly occurs from the following examples:

Federal Regulation

Federal Regulation

Sarbanes-Oxley Act (SOX): After the increase of corporate fraud in the early 2000's, the U.S. Congress passed the Sarbanes-Oxley Act in 2002 to protect investors from the possibility of fraudulent accounting practices by corporations.

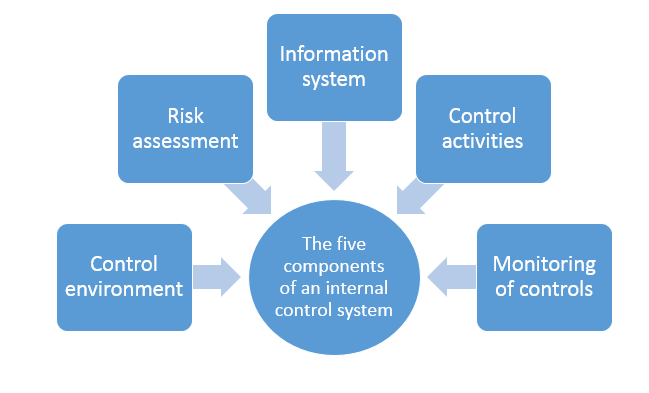

Sarbanes-Oxley applies only publicly held companies; although all companies have been impacted by Sarbanes-Oxley. The law emphasizes the importance of effective internal control. Internal control is defined as the procedures and processes used by a company to:

- Safeguard its assets.

- Process information accurately.

- Ensure compliance with laws and regulations.

The Sarbanes Oxley Act requires all financial reports to include an Internal Controls Report. This shows that a company's financial data accurate and adequate controls are in place to safeguard financial data. Year-end financial disclosure reports are also a requirement. A SOX auditor is required to review controls, policies, and procedures during a Section 404 audit.

Internal Regulations

Internal Control

Objectives of Internal Control

The objectives of internal control are to provide reasonable assurance that:

- Assets are safeguarded and used for business purposes.

- Business information is accurate.

- Employees and managers comply with laws and regulations.

Internal control can safeguard assets by preventing theft, fraud, misuse, or misplacement of funds and inventory. A serious concern of internal control is preventing employee fraud. Employee fraud is the intentional act of deceiving an employer for personal gain. Such fraud may range from minor overstating of a travel expense report to stealing millions of dollars. Employees stealing from a business often adjust the accounting records in order to hide their fraud. Thus, employee fraud usually affects the accuracy of business information. Accurate information is necessary to successfully operate a business. Businesses must also comply with laws, regulations, and financial reporting standards. Examples of such standards include environmental regulations, safety regulations, and generally accepted accounting principles (GAAP).

Control Environment

Control Environment

The control environment is the overall attitude of management and employees about the importance of controls. Three factors influencing a company's control environment are as follows:

- Management's philosophy and operating style

- The company's organizational structure

- The company's personnel policies

Management's philosophy and operating style relates to whether management emphasizes the importance of internal controls. An emphasis on controls and adherence to control policies creates an effective control environment. In contrast, overemphasizing operating goals and tolerating deviations from control policies creates an ineffective control environment.

All businesses face risks such as changes in customer requirements, competitive threats, regulatory changes, and changes in economic factors. Management should identify such risks, analyze their significance, assess their likelihood of occurring, and take any necessary actions to minimize them.

Control Activities

Control activities provide reasonable assurance that business goals will be achieved, including the prevention of fraud. Control procedures, which constitute one of the most important elements of internal control, include the following:

- Competent personnel, rotating duties, and mandatory vacations

- Separating responsibilities for related operations

- Separating operations, custody of assets, and accounting

Competent Personnel, Rotating Duties, and Mandatory Vacations

A successful company needs competent employees who are able to perform the duties that they are assigned. Procedures should be established for properly training and supervising employees. It is also advisable to rotate duties of accounting personnel and mandate vacations for all employees. In this way, employees are encouraged to adhere to procedures. Cases of employee fraud are often discovered when a long-term employee, who never took vacations, missed work because of an illness or another unavoidable reason.

Separating Responsibilities for Related Operations

The responsibility for related operations should be divided among two or more persons. This decreases the possibility of errors and fraud.

Separating Operations, Custody of Assets, and Accounting

The responsibilities for operations, custody of assets, and accounting should be separated. In this way, the accounting records serve as an independent check on the operating managers and the employees who have custody of assets. For example, the person that handles cash should not be the same person that record cash transactions into the journals.

Proofs and Security Measures

Proofs and security measures are used to safeguard assets and ensure reliable accounting data. Proofs involve procedures such as authorization, approval, and reconciliation. For example, an employee planning to travel on company business may be required to complete a “travel request” form for a manager's authorization and approval.

- Documents used for authorization and approval should be prenumbered, accounted for, and safeguarded. Prenumbering of documents helps prevent transactions from being recorded more than once or not at all. In addition, accounting for and safeguarding prenumbered documents helps prevent fraudulent transactions from being recorded. For example, blank checks are prenumbered and safeguarded. Once a payment has been properly authorized and approved, the checks are filled out and issued.

- Reconciliations are also an important control. Later in this chapter, the use of bank reconciliations as an aid in controlling cash is described and illustrated.

- Security measures involve measures to safeguard assets. For example, cash on hand should be kept in a cash register or safe. Inventory not on display should be stored in a locked storeroom or warehouse. Accounting records such as the accounts receivable subsidiary ledger should also be safeguarded to prevent their loss. For example, electronically maintained accounting records should be safeguarded with access codes and backed up so that any lost or damaged files could be recovered if necessary.

Monitoring

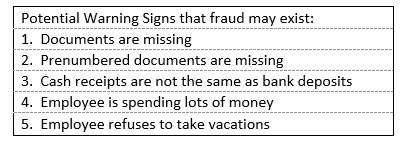

Monitoring the internal control system is used to locate weaknesses and improve controls. Monitoring often includes observing employees' behavior and the accounting system for indicators of control problems. Some such indicators are Warning Signs of Internal Control Problems. Other potential warning signs are:

Fraud Tips

Tips on Preventing Employee Fraud in Small Companies

- Do not have the same employee write company checks and keep the books. Look for payments to vendors you don't know or payments to vendors whose names appear to be misspelled.

- If your business has a computer system, restrict access to accounting files as much as possible. Also, keep a backup copy of your accounting files and store it at an off-site location.

- Be wary of any employee working in finance that declines to take vacations. They may be afraid that a replacement will uncover fraud.

- Require and monitor supporting documentation (such as vendor invoices) before signing checks.

- Track the number of credit card bills you sign monthly.

- Limit and monitor access to important documents and supplies, such as blank checks and signature stamps.

- Check W-2 forms against your payroll annually to make sure you're not carrying any fictitious employees.

- Rely on yourself, not on your accountant, to spot fraud.

Source: Steve Kaufman, “Embezzlement Common at Small Companies,” Knight-Ridder Newspapers, reported in Athens Daily News/Athens Banner-Herald, March 10, 1996, p. 4D.

Cash and Cash Equivalents

Cash

Most companies use checking accounts to handle their cash transactions. The company deposits its cash receipts in a bank checking account and writes checks to pay its bills. Keep in mind, a bank account is an asset to the company BUT to the bank your account is a liability because the bank owes the money in your bank account to you. For this reason, in your bank account, deposits are credits (remember, liabilities increase with a credit) and checks and other reductions are debits (liabilities decrease with a debit).

The bank sends the company a statement each month. The company checks this statement against its records to determine if it must make any corrections or adjustments in either the company’s balance or the bank’s balance. A bank reconciliation is a schedule the company (depositor) prepares to reconcile, or explain, the difference between the cash balance on the bank statement and the cash balance on the company’s books. The company prepares a bank reconciliation to determine its actual cash balance and prepare any entries to correct the cash balance in the ledger.

Certificates of Deposit

A certificate of deposit (CD) is an interest-bearing deposit that can be withdrawn from a bank at will (demand CD) or at a fixed maturity date (time CD). Only demand CDs that may be withdrawn at any time without prior notice or penalty are included in cash. Cash does not include postage stamps, IOUs, time CDs, or notes receivable.

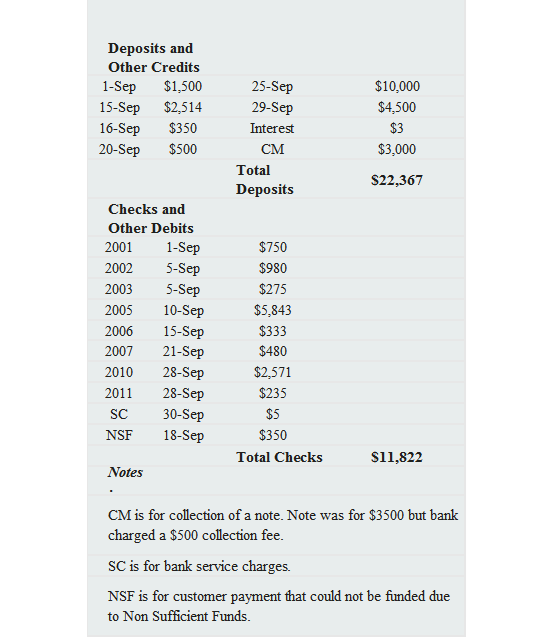

Bank Statment

Bank Statement

A bank statement is a record of your bank account transactions, typically for one month, prepared by the bank. In the Deposit and credits section, you see the deposits made into the account and a CM which is a collection of a note (see note at bottom of statement) and interest the bank has paid to your account. In the Checks and debits section, you see the individual checks that have been processed by the bank and you also see SC for a bank service charge on your account as well as a NSF (stands for Non Sufficient Funds) and means we made a deposit from a customer but the customer did not have enough money to pay the check (bounced check). A bank statement looks like this:

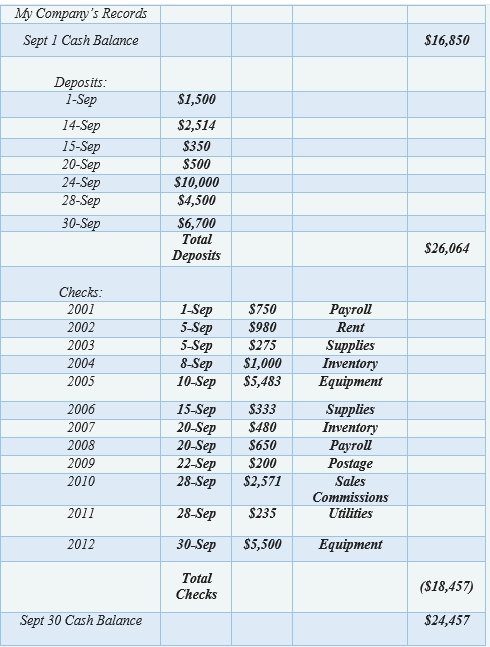

Company's Records

Company’s Records

The company’s records (or books) refers to the general ledger posting and can be in the form of cash disbursement journal, cash receipt journal, cash general ledger postings or lists of cash transactions. An example of a cash listing is:

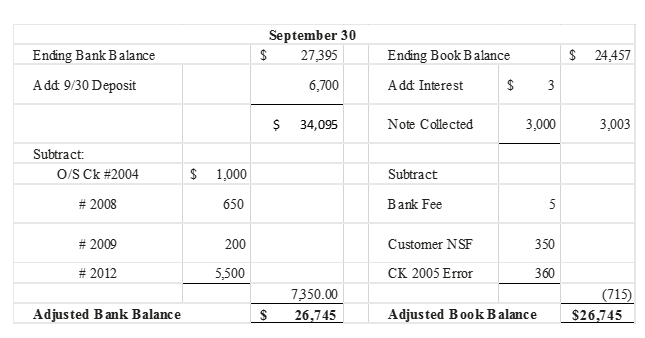

The bank balance on September 30 is $27,395 but according to our records, the ending cash balance is $24,457. We need to do a bank reconciliation to find out why there is a difference.

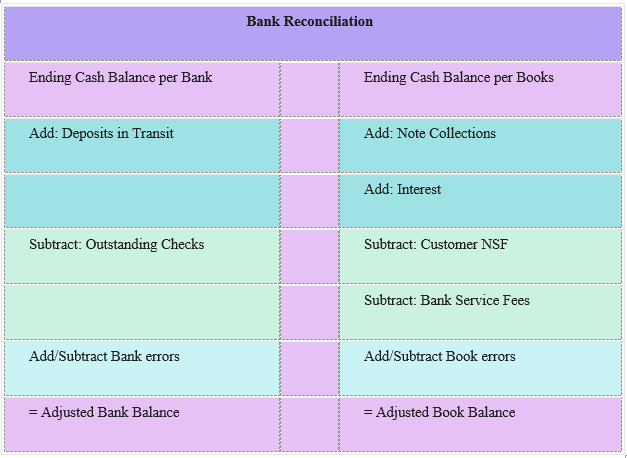

Bank Reconciliation

Bank Reconciliation

A bank reconciliation compares the bank statement and our company’s records and reconciles or balances to two account balances. How does it do this? There are several items of information we can get by comparing the bank statement to our records — anything that doesn’t match or doesn’t exist on both places is called a reconciling item. A reconciling item will be added or subtracted to the bank or book side of the reconciliation. The following table will give you some examples of how these reconciling items apply in a bank reconciliation:

Bank Reconciliation Information

Deposits

Compare the deposits listed on the bank statement with the deposits on the company’s books. To make this comparison, place check marks in the bank statement and in the company’s books by the deposits that agree. Then determine the deposits in transit. A deposit in transit is typically a day’s cash receipts recorded in the depositor’s books in one period but recorded as a deposit by the bank in the succeeding period. The most common deposit in transit is the cash receipts deposited on the last business day of the month. Normally, deposits in transit occur only near the end of the period covered by the bank statement. For example, a deposit made in a bank’s night depository on May 31 would be recorded by the company on May 31 and by the bank on June 1. Thus, the deposit does not appear on a bank statement for the month ended May 31. Also check the deposits in transit listed in last month’s bank reconciliation against the bank statement. Immediately investigate any deposit made during the month but missing from the bank statement (unless it involves a deposit made at the end of the period).

Paid checks

If canceled checks (a company’s checks processed and paid by the bank) are returned with the bank statement, compare them to the statement to be sure both amounts agree. Then, sort the checks in numerical order. Next, determine which checks are outstanding. Outstanding checks are those issued by a depositor but not paid by the bank on which they are drawn. The party receiving the check may not have deposited it immediately. Once deposited, checks may take several days to clear the banking system. Determine the outstanding checks by comparing the check numbers that have cleared the bank with the check numbers issued by the company. Use check marks in the company’s record of checks issued to identify those checks returned by the bank. Checks issued that have not yet been returned by the bank are the outstanding checks. If the bank does not return checks but only lists the cleared checks on the bank statement, determine the outstanding checks by comparing this list with the company’s record of checks issued. Sometimes checks written long ago are still outstanding. Checks outstanding as of the beginning of the month appear on the prior month’s bank reconciliation. Most of these have cleared during the current month; list those that have not cleared as still outstanding on the current month’s reconciliation.

Bank debit and credit memos

Verify all debit and credit memos on the bank statement. Debit memos reflect deductions for such items as service charges, NSF checks, safe-deposit box rent, and notes paid by the bank for the depositor. Credit memos reflect additions for such items as notes collected for the depositor by the bank and wire transfers of funds from another bank in which the company sends funds to the home office bank. Check the bank debit and credit memos with the depositor’s books to see if they have already been recorded. Make journal entries for any items not already recorded in the company’s books.

Bank Errors

Sometimes banks make errors by depositing or taking money out of your account in error. You will need to contact the bank to correct these errors but will not record any entries in your records because the bank error is unrelated to your records.

Book Errors

List any Book errors. A common error by depositors is recording a check in the accounting records at an amount that differs from the actual amount. For example, a $47 check may be recorded as $74. Although the check clears the bank at the amount written on the check ($47), the depositor frequently does not catch the error until reviewing the bank statement or canceled checks.

Deposits in transit, outstanding checks, and bank service charges usually account for the difference between the company’s Cash account balance and the bank balance.

Bank Reconciliation Expample

After comparing the bank statement and records of My Company, you should have identified the following reconciling items:

- Deposit in transit dated 9/30 for $6,700.

- Outstanding checks #2004, 2008, 2009, 2012.

- Interest paid by the bank $3.

- Note collected by bank $3500 less $500 fee

- Bank service charge $5

- Customer NSF $350

- Error in Check #2005 correctly processed by bank as $5,843 but recorded in our records as $5,483. This is a difference of $360 (5,843 – 5,483) and since we did not take enough cash we need to reduce cash by $360.

Using the chart provided above and the reconciling items, the bank reconciliation would appear as follows:

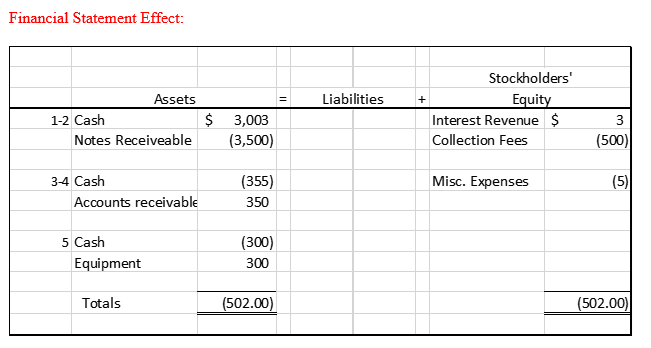

When the bank and book are in agreement, you are almost finished. On the bank side of the reconciliation, you do not need to do anything else except contact the bank if you notice any bank errors. On the book side, you will need to do journal entries for each of the reconciling items.

Adjusting Entries for Book side Reconciling Items

The ending cash balance on the general ledger is reconciled to the adjusted bank statement balance. When a company maintains more than one checking account, it must reconcile each account separately with the balance on the bank statement for that account. The depositor should also check carefully to see that the bank did not combine the transactions of the two accounts.

Within the internal control structure, segregation of duties is an important way to prevent fraud. One place to segregate duties is between the cash disbursement cycle and bank reconciliations. To prevent collusion among employees, the person who reconciles the bank account should not be involved in the cash disbursement cycle. Also, the bank should mail the statement directly to the person who reconciles the bank account each month. Sending the statement directly limits the number of employees who would have an opportunity to tamper with the statement.

Chapter 7: Long-term Assets

In this section, we will look at the accounting treatment for plant assets, natural resources and intangible assets. Investments will be covered in other chapters. Property, plant, and equipment (fixed assets or operating assets) compose more than one-half of total assets in many corporations. These resources are necessary for the companies to operate and ultimately make a profit. It is the efficient use of these resources that in many cases determines the amount of profit corporations will earn.

- Define, classify, and account for the cost of fixed assets.

- Compute depreciation using the straight-line and double-declining-balance methods.

- Describe the accounting for the disposal of fixed assets.

- Describe the accounting for natural resources.

- Describe the accounting for intangible assets.

- Describe the reporting of fixed assets, natural resources, and intangible assets on the income statement and balance sheet.

Long-term Assets Section of the Balance Sheet

On a classified balance sheet, the asset section contains: (1) current assets; (2) property, plant, and equipment; and (3) other categories such as intangible assets and long-term investments. Previous chapters discussed current assets. Property, plant, and equipment are often called plant and equipment or simply plant assets. Plant assets are long-lived assets because they are expected to last for more than one year. Long-lived assets consist of tangible assets and intangible assets. Tangible assets have physical characteristics that we can see and touch; they include plant assets such as buildings and furniture, and natural resources such as gas and oil. Intangible assets have no physical characteristics that we can see and touch but represent exclusive privileges and rights to their owners.

Plant Assets

Plant Assets

To be classified as a plant asset, an asset must:

- (1) be tangible, that is, capable of being seen and touched;

- (2) have a useful service life of more than one year;

- and (3) be used in business operations rather than held for resale.

Common plant assets are buildings, machines, tools, and office equipment. On the balance sheet, these assets appear under the heading “Property, plant, and equipment”.

Property, plant, and equipment (fixed assets or operating assets) compose more than one-half of total assets in many corporations. These resources are necessary for the companies to operate and ultimately make a profit. It is the efficient use of these resources that in many cases determines the amount of profit corporations will earn.

Initial recording of plant assets

When a company acquires a plant asset, accountants record the asset at the cost of acquisition (historical cost). When a plant asset is purchased for cash, its acquisition cost is simply the agreed on cash price. This cost is objective, verifiable, and the best measure of an asset’s fair market value at the time of purchase. Fair market value is the price received for an item sold in the normal course of business (not at a forced liquidation sale). Even if the market value of the asset changes over time, accountants continue to report the acquisition cost in the asset account in subsequent periods.

The acquisition cost of a plant asset is the amount of cost incurred to acquire and place the asset in operating condition at its proper location. Cost includes all normal, reasonable, and necessary expenditures to obtain the asset and get it ready for use. Acquisition cost also includes the repair and reconditioning costs for used or damaged assets as longs as the item was not damaged after purchase. Unnecessary costs (such as traffic tickets or fines or repairs that occurred after purchase) that must be paid as a result of hauling machinery to a new plant are not part of the acquisition cost of the asset.

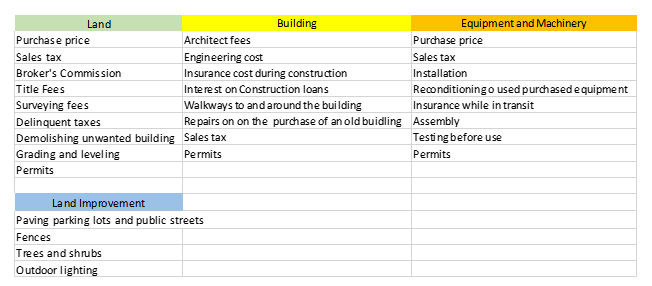

Purchasing Land

Land

The cost of land includes its purchase price and other many other costs including:

- real estate commissions,

- title search and title transfer fees,

- title insurance premiums,

- existing mortgage note or unpaid taxes (back taxes) assumed by the purchaser,

- costs of surveying, clearing, and grading;

- and local assessments for sidewalks, streets, sewers, and water mains.

- Sometimes land purchased as a building site contains an unusable building that must be removed.